Millions of Americans find themselves unable to save money each month, and up to 35% occasionally miss loan payments.

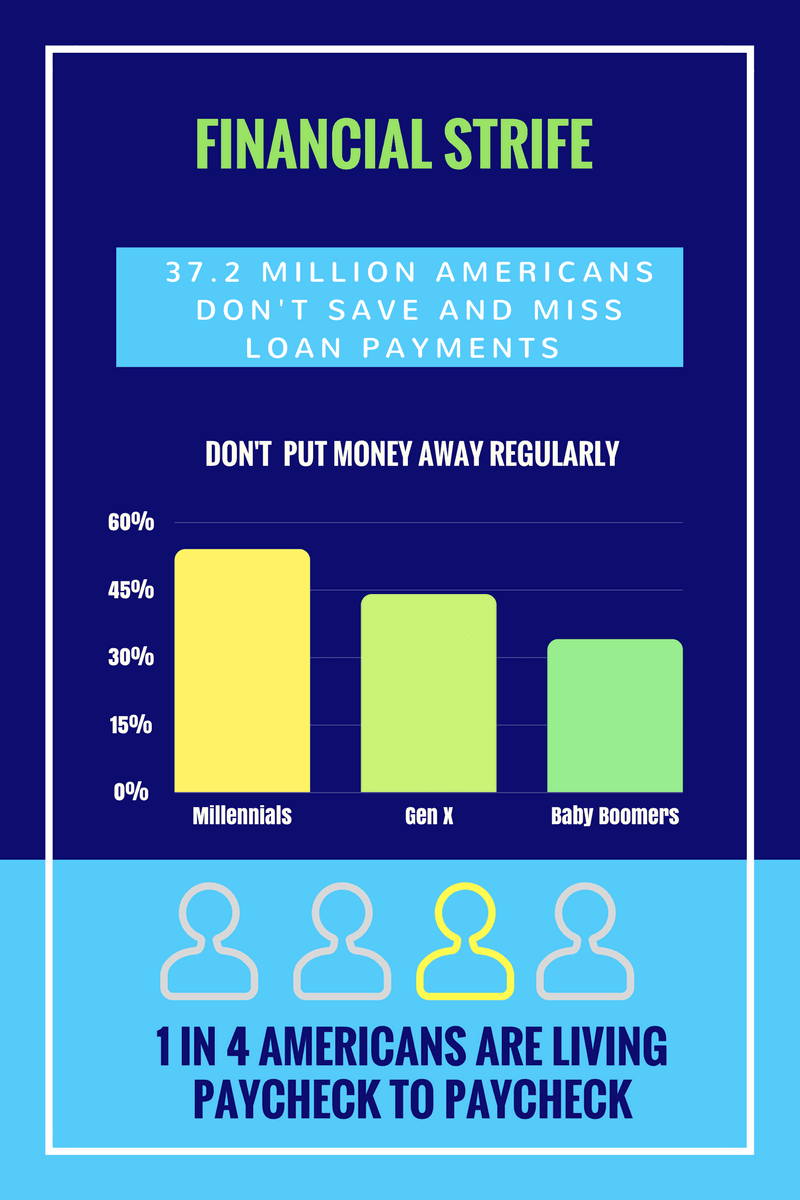

Americans are having a hard time saving for the future. According to personal finance comparison site finder.com, not only are 37.2 million Americans unable to save monthly, but they are also missing loan payments. That number is equal to 15% of the US population.

Those fortunate enough to be in a position to make good on their loan payments aren’t necessarily in the clear. One in four Americans live paycheck to paycheck each month without putting any savings away.

The breakdown

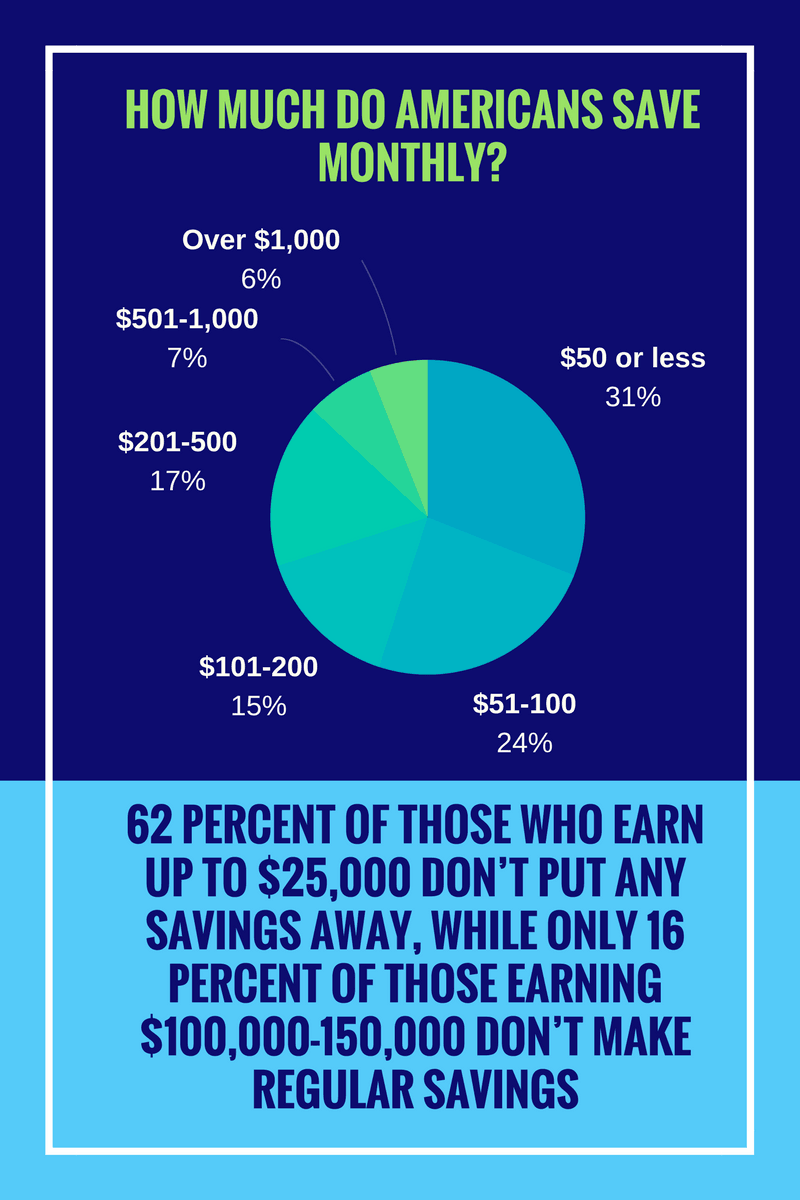

It makes sense that those who earn less save less. If you earn up to $25,000 a year, it’s likely that you’re part of the 62% who aren’t making monthly deposits to your piggy bank. Only 16% of people in the six-figure club earning $100,000 to $150,000 are spending their whole wad, with the remaining 84% saving for a rainy day.

Making regular savings when you are employed is hard enough. But those outside of the workforce are the least likely to make regular savings. That said, 61% of students say they are able to put something away regularly, while 48% of retirees do so despite not working.

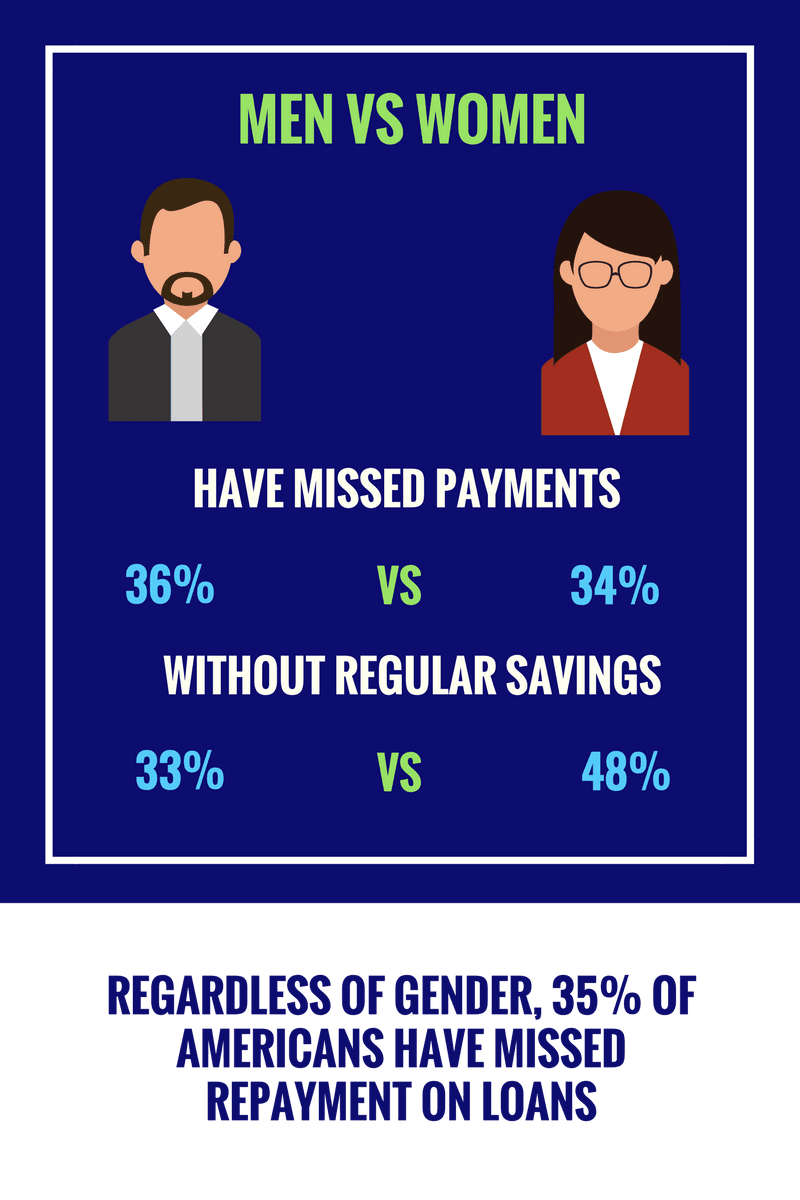

Only 52% of women keep regular savings, compared with 67% of men who do. This is worrying for mothers and women, who pay more for products in “pink taxes” and face wage discrepancies when compared with their male counterparts.

Baby boomers are the best savers, with two out of three (66%) regularly storing cash, followed by Generation Xers, of whom more than half (56%) save monthly.

Fewer jobs, increased college debt and the fact that people generally earn less at the start of their careers may be contributing factors for millennials, who have the hardest time saving — over half (54%) admit that they don’t put money away regularly.

Those who are able to stash at least something away average $343 a month. The majority of the fiscally able put away $100 or less a month. One in three Americans put away $50 or less, while 24% afford $50 to $100 in savings monthly. Only 6% are able to really throw it at the bank, saving at least $1,000 a month.

Facing debts

Accumulating wealth is difficult when you have to worry about making loan payments, not to mention the costly undertaking of being alive. In fact, 35% of Americans have missed a repayment on credit cards, mortgages, car loans or short-term payday loans.

Credit card payments are most likely to be skipped: 27% of Americans admit to missing at least one. Personal loans and car loans are next, with 9% dodging these payments, and 8% of Americans are missing out on mortgages.

While skipping a mortgage payment may sound terrifying, missing a short-term loan can leave you owing more money more quickly due to penalty fees and exorbitant interest rates. Six percent of Americans admit to skipping this kind of payment.

What to do?

Debt can get out of hand quickly. Accumulating interest rates and penalty fees lurk behind every statement, so it’s a good plan to pay on time and avoid taking on extra debt. Combining this plan with saving even a little every month can set you up for success.

Avoid falling behind

Get financially literate. Many websites are dedicated to helping people understand personal finance, including finder.com. Understanding your debts and interest payments will help you see where your money is going and shop for better rates.

List your expenses and payments. Debit and credit cards make it easy to lose track of how much you’re spending. Understanding where it goes can make you more aware of its value.

Consolidate your debt. If you’re making small payments on student loans or credit cards, you may be able to refinance or find a better interest rate to pay off your balance sooner. Compare potential savings with balance transfer offers from finder.com.

Tips for saving

Skip the fancy coffee. No need to hold out everyday, but turn that indulgence into savings at least twice a week. You’ll look forward to your muffin or latte on those special days and save several hundred dollars a year.

Out of sight, out of mind. Deposit a reasonable amount — however small — into your savings account every month. Many employers can set up direct deposit so that you don’t even see it in your paycheck. Just be sure to turn down the debit card that comes with your account to avoid temptation.

Ask yourself if you really need it. Visualize how every nonessential item you want to buy will fit into your life — whether immediately, in a month, or in six months. You might find that your eyes are bigger than your needs, giving you the flexibility to splurge on the things you really want.

For all media inquiries, please contact:

Richard Laycock, Insights editor and senior content marketing manager

Michelle Hutchison is chief operating officer at Schebesta Ventures. She's an award-winning public relations pro and advisory board member, and has held multiple roles in Finder including global head of communication and compliance officer for Finder Ventures, and global head of communication for Finder. Michelle started at Finder in 2013 as the Australian head of PR and money expert. With more than a decade of experience in public relations, Michelle was formerly a journalist and editor, and has written for numerous publications including The Guardian, The Sydney Morning Herald, Mamamia and New Idea.

See full bio

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.