Finder maintains full editorial independence to ensure for our readers a fair assessment of the products, brands, and services we write about. That independence helps us maintain our reader's trust, which is what keeps you coming back to our site. We uphold a rigorous editorial process that ensures what we write and publish is fair, accurate, and trustworthy — and not influenced by how we make money.

We're committed to empowering our readers to make sound and often unfamiliar financial decisions.

We break down and digest information information about a topic, product, brand or service to help our readers find what they're looking for — whether that's saving money, getting better rewards or simply learning something new — and cover any questions you might not have even thought of yet. We do this by leading with empathy, leaning on plain and conversational language that speaks directly, without speaking down.

If you’re gearing up to walk away from the workforce, you’ll need to know your full retirement age. In April 2021, 48 out of 62 million people who received Social Security were aged 65 or older. But age 65 isn’t the full retirement age for everyone. And for some Americans, retiring early could mean less money in retirement.

What is the full retirement age?

Full retirement age is the age that you can start receiving or drawing from your retirement accounts. But many refer to full retirement age specifically as when they can claim unreduced Social Security benefits. In 1983, the Social Security Administration gradually increased the full retirement age for Social Security benefits from 65 to 67. Here’s your full retirement age based on your birth year.

Birth year

Full retirement age

1943-1954

66

1955

66 and 2 months

1956

66 and 4 months

1957

66 and 6 months

1958

66 and 8 months

1959

66 and 10 months

1960 and later

67

If you were born on January 1, your benefits are based on the previous year.

How your retirement age affects your Social Security

It’s possible to retire and start collecting your Social Security payments at 62. But if you retire before your full retirement age, your benefits are permanently reduced. Here’s how much you might lose if you file for Social Security benefits early at age 62.

Birth year

Full retirement age

Percent loss in benefit amount

1943-1954

66

25%

1955

66 and 2 months

25.83%

1956

66 and 4 months

26.67%

1957

66 and 6 months

27.5%

1958

66 and 8 months

28.33%

1959

66 and 10 months

29.17%

1960 and later

67

30%

Fortunately, you’ll forfeit less of your Social Security payment amount every month you inch closer to your full retirement age. For example, here’s a quick glimpse of your benefits reduction if you’re born in 1960 or later and retire between age 62 and your full retirement age of 67.

Early filing age

Percentage loss in benefit amount

62

30%

63

25%

64

20%

65

13.9%

66

6.7%

67

0%

If you claim Social Security benefits early and continue to work, your earned income can reduce your payment. This is known as the Earnings Test.

Essentially, for every two dollars that you make over a specific threshold, one dollar of your benefit will be withheld. The withholding rate is a bit kinder if you’re reaching your full retirement age that year. To find out how your earnings can affect your monthly benefit, use the Social Security Administration’s Retirement Earnings Test Calculator.

Once you reach your full retirement age, you’re exempt from the Retirement Earnings Test.

What happens if you work after the full retirement age?

If you delay retirement and postpone claiming Social Security, you stand to increase your benefits every month until age 70. For those born in 1960 or later, here’s how much you could boost your monthly benefit.

Delayed benefit filing age

Percent increase in benefit amount

67

0%

68

8%

69

16%

70

24%

Do you get more in Social Security by retiring early or delaying retirement?

Arguments can be made that if you retire early at age 62, you get more Social Security payments than if you delay retirement to age 70 — even with the reduced monthly benefit. While many factors go into how much Social Security will pay out in your lifetime, here’s how the math could play out.

Let’s say you’re entitled to a monthly retirement benefit of $1,000. If you were born in 1960 or later and retire at 62, your retirement benefit would be reduced to $700 — a reduction of 30%. If you continue to collect Social Security until the average life expectancy of age 78, you’d receive a total of 192 monthly payments or $134,400 (192 x $700).

On the other hand, if you delay retirement benefits until 70, your payment could increase to $1,240 — an increase of 24%. If you secure payments until age 78, you’d get a total of 96 monthly benefits or $119,040 (96 x $1,240). While retiring early cuts your monthly payment in this situation, you’ll receive more money over time.

How to factor Social Security into retirement planning

Social Security is generally designed only to replace about 40% of your pre-retirement earnings. Many people supplement their retirement plan with other income sources, including individual retirement accounts (IRA) and 401(k)s. So when considering when to retire, your Social Security full retirement age should only be one factor. Other considerations include when you become eligible to receive payments from your other retirement earnings without penalty, whether you can afford to retire early and your personal circumstances that may delay walking away from your job.

Take distributions from your retirement plan, including IRAs, 401(k)s and pension plans, without incurring the 10% early withdrawal tax if you’re age 59 1/2. Keep in mind that the withdrawal is subject to income tax, which is unavoidable unless you have a Roth IRA or Roth 401(k) account.

You may also face an additional 25% tax if you withdraw from a SIMPLE IRA within the first two years of joining the plan. So you might consider postponing retirement — even if you’re 59 1/2 — to avoid this extra penalty.

How much do you think you ll need to have saved to retire comfortably?

Response

% of Americans

Less than $250k

20%

$750k - $999K

14%

$500k - $749k

16%

$5 million +

4%

$4 - $4.99 million

1%

$3 - $3.99 million

2%

$250k - $499k

19%

$2 - $2.99 million

4.38%

$1.5 - $1.99 million

6.20%

$1 - $1.49 million

14.46%

Source: Finder survey by Qualtrics of 2,033 Americans

One in five Americans (20%) think that they will be able to live on $250K or less in retirement, while a combined 31% say they will need more than $1 million.

Compare retirement accounts

7 of 7 results

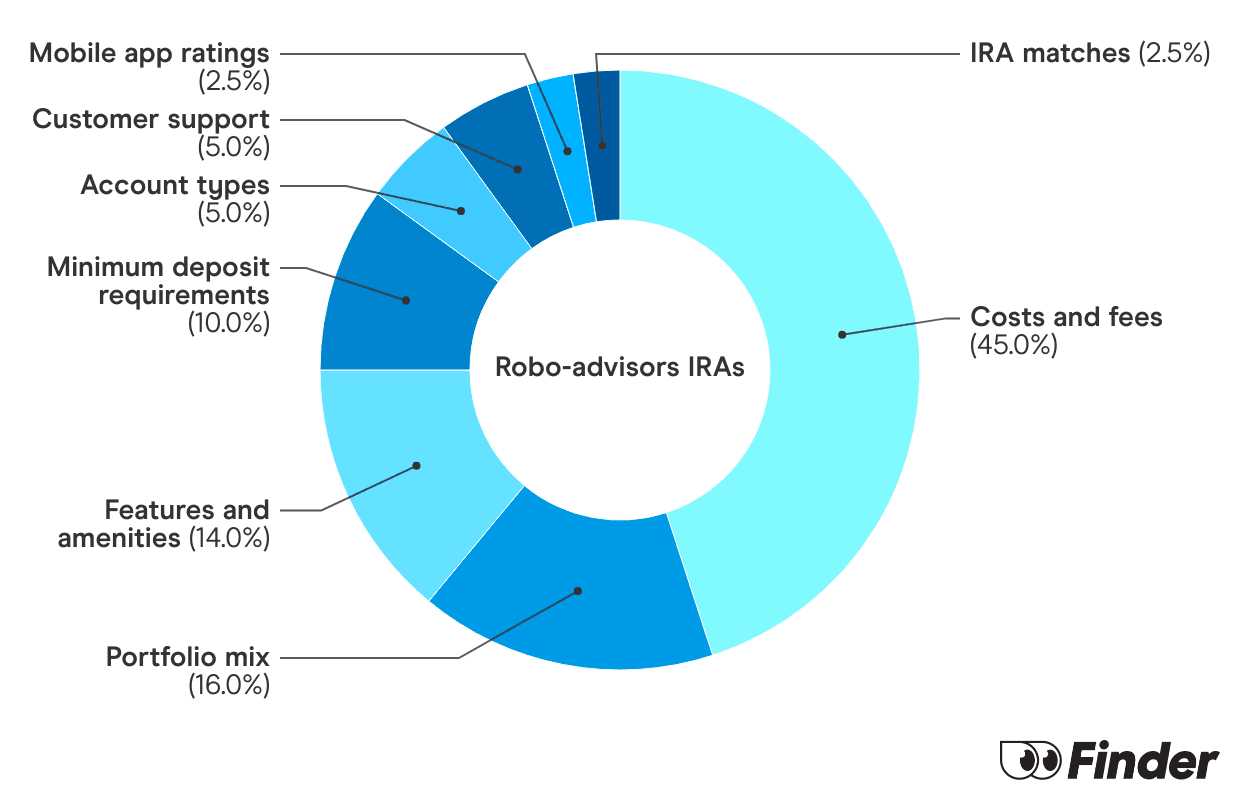

What is the Finder Score?

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Bottom line

Your full retirement age is when you’re entitled to receive full Social Security benefits. You might be able to retire earlier, but your monthly check will be smaller. Since Social Security is likely only a portion of your retirement income, consider other retirement plans to help supplement your retirement cash flow.

Kimberly Ellis is a personal finance writer at Finder, specializing in banking and financial literacy. After teaching in public and private schools, Kimberly zeroed in on personal financial education to help families and kids develop lifelong money skills. She hails from New York City, graduating summa cum laude from Queens College with a BA in elementary education and mathematics, as well as a New York State teaching certificate. She’s also an aspiring polyglot, always in a book and forever on the hunt for the perfect classic red lipstick.

See full bio

Kimberly's expertise

Kimberly

has written

56

Finder guides across topics including:

Here’s how retirement savings accounts work and how to compare your options.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.