Finder makes money from featured partners, but editorial opinions are our own.

Advertiser disclosure

Roth IRA vs. savings account: How do they compare?

Key differences in purpose, tax advantages and investment options.

Roth individual retirement accounts (IRAs) and savings accounts are two account options for individuals looking to save and grow their money.

However, these two accounts vary greatly in terms of tax advantages, available asset types and, most importantly, purpose. Find out more about how these accounts differ to see which is right for you.

| Roth IRA | Savings account | |

|---|---|---|

| Where to open | Brokers, banks or other financial institutions | Banks, credit unions and other financial institutions |

| Investment options | All assets are permitted inside an IRA except collectibles and life insurance The IRA custodian determines available investment options | Cash deposits |

| Income limits | Individuals filing as single and head of household. Contribute up to $7,000 if your 2025 modified adjusted gross income (MAGI) is under $150,000; individuals with a MAGI above $150,000 can contribute a reduced amount until contributions are phased out upon reaching a MAGI of $165,000 Married couples filing jointly. | None |

| Contribution limits | $7,000 for those under age 50 $8,000 for those age 50 and over | None |

| Eligibility requirements | No age requirements, but you need earned income to contribute Income limits apply | None |

| Who can contribute | Anyone with earned income so long as their income doesn’t exceed a certain threshold | N/A |

| Tax advantages | Earnings grow tax-free Qualified withdrawals are tax-free | None |

| Withdrawal restrictions | Withdrawals of earnings before age 59.5 from a Roth IRA you’ve held less than five years will incur taxes and penalties (exceptions apply) Withdrawals of earnings after age 59.5 from a Roth IRA you’ve had more than five years will be subject to taxes but not penalties | The Federal Reserve suspended the six-transaction rule in Regulation D in 2020, though individual banks may impose withdrawal limits |

| Required minimum distributions (RMDs) | No RMDs | None |

| FDIC insurance | Roth IRAs that contain bank deposits such as certificates of deposit (CDs), savings accounts or money market accounts are insured up to $250,000 | Deposits are automatically insured to at least $250,000 per depositor, per insured bank |

| SIPC insurance | SIPC insures cash and securities up to $500,000 at SIPC-member brokers | None |

| Pros |

|

|

| Cons |

|

|

| Learn more about Roth IRAs | Learn more about savings accounts |

Roth IRAs and savings accounts have different purposes, so one is not necessarily better than the other. A Roth IRA is a tax-advantaged retirement account meant for long-term investing, while a savings account is a deposit account for cash.

A Roth IRA may be a good option if you:

Consider a savings account if you:

Roth IRAs and savings accounts can both be used to save money for long-term goals, and both can earn interest. However, the structure of these accounts will change the way you use them to reach your goals. For example, Roth IRAs offer tax advantages for saving for retirement. Savings accounts do not.

Open a Roth IRA through banks, financial institutions or brokers like Fidelity and Charles Schwab or with stock trading apps like SoFi Invest® and Robinhood.

Open a savings account at banks, credit unions and online financial services companies.

While Roth IRAs and savings accounts are great options to help you save for financial goals, other accounts may be more appropriate depending on those goals:

Narrow down top brokers by annual fee, stock trade fee and more to find the best for your budget and financial goals.

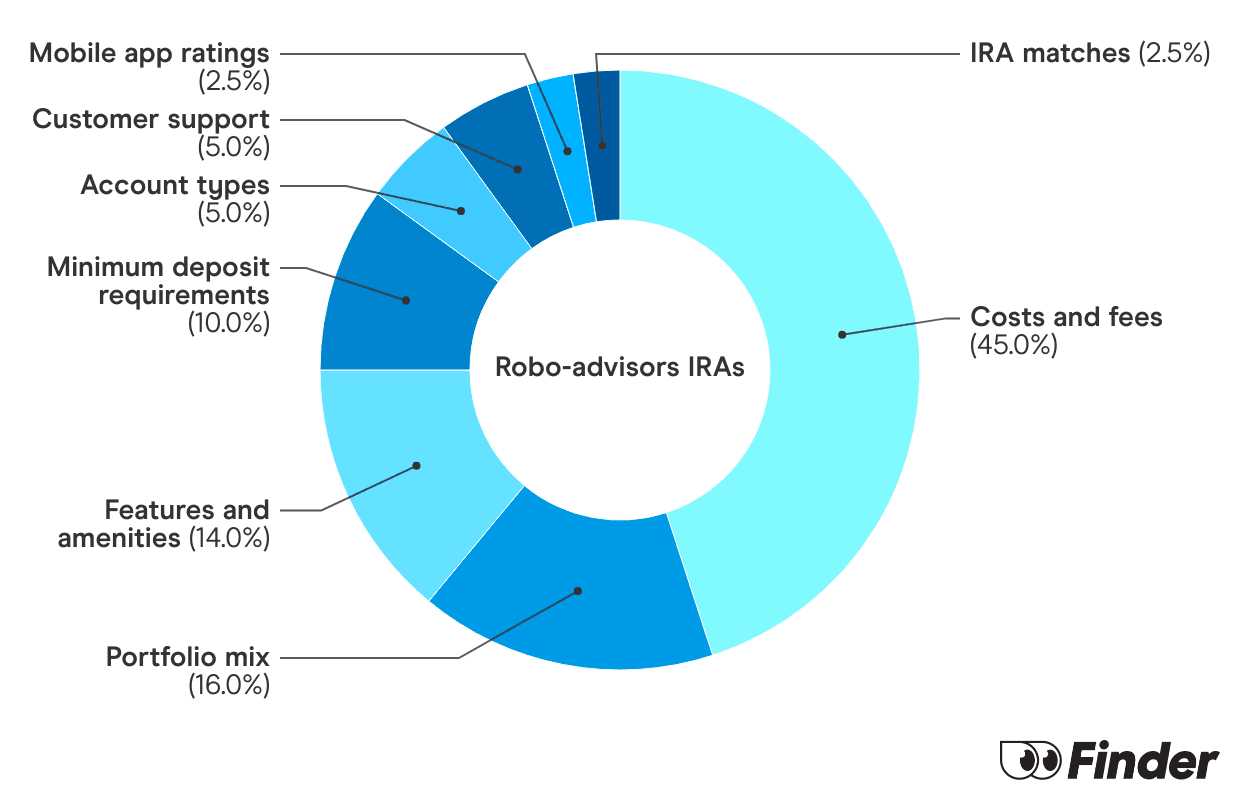

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Your goals will determine whether it’s better to put money in a savings account or a Roth IRA. If you want to save specifically for retirement, a Roth IRA may be the better option because it offers tax benefits. If you’re saving for short- or long-term goals — other than retirement — where you need easy access to your funds, a savings account may be the better option.

Some disadvantages of a Roth IRA include no tax deductions on contributions and penalties for early withdrawals.

The amount a Roth IRA grows over 20 years depends on your investment choices and market conditions.

Three advantages of putting money in a Roth IRA include tax-free withdrawals in retirement, tax- and penalty-free withdrawals on contributions at any time and the ability to invest in a range of asset types.

Get up to a 3% IRA match with Robinhood and Acorns or a 1% IRA match with Public. See how to qualify here.

Explore the pros and cons of the best SEP IRAs and learn how to open one of these accounts.

What you need to know about SEP IRAs and how these retirement accounts work.

Check out the best Roth IRA providers overall — with guidance on which ones tend to work best for different investing styles.

Check out the best IRA providers overall — with guidance on which ones tend to work best for different investing styles.

The rush of turning $19,500 into $1 million can be enticing, but it’s not always the best idea.

Learn the differences between a Roth IRA and a traditional IRA.

Learn how Roth IRAs work and who qualifies to open one.

Need a quick influx of cash? Before you dig into your retirement funds, consider these drawbacks.

Here’s how retirement savings accounts work and how to compare your options.