There’s no universal retirement number where you can say goodbye to your job and head towards warmer weather without worrying about running out of money. While the average retirement age is generally 65 for men and 63 for women, according to the Center for Retirement Research at Boston College, this isn’t a magic number for everyone. Instead, your retirement age relies heavily on when you’ll get Social Security benefits, your expenses and how much you have saved in your nest egg.

How to calculate your retirement number

The first step to determining when you can retire is figuring out when you become eligible for full Social Security retirement benefits. The Social Security Administration has a convenient retirement age calculator that can tell you what age you’ll become eligible for unreduced payments. Although you can start collecting retirement benefits as early as age 62, your payments will be reduced. For example, if you were born in 1960 or later and retire at 62, you’d only receive 70% of the entire Social Security benefit amount. At age 65, you may get 86.7%, but if you wait until age 67, you will get the full amount.

Rules of thumb

Your retirement age can vary for many reasons, including health, job availability and simply whether you can afford to stop working. When determining when you should retire, consider how much you’ll need to support yourself in retirement. There are two primary ways to calculate how much money you’ll need to retire: Based on income The income method is a straightforward way to calculate how much you need to retire. Take your current income and multiply it by 10, according to Fidelity Investments. For example, someone who makes $60,000 a year may need to save $600,000 to retire at age 67, whereas someone accustomed to making $80,000 a year might need $800,000 to retire. A few fundamental assumptions for this calculation include:

Social Security benefits. This calculation takes into account that you’ll receive full Social Security retirement benefits. If you’re born in 1960 or later, this means retiring at age 67.

No pension. The target retirement number assumes you won’t get any pension income.

45% income replacement. This method presumes that you’ll only use 45% of your pre-retirement income, excluding Social Security.

Based on expenses The expense method is a bit more labor-intensive. Your retirement number is based on covering your expenses in retirement. Here’s how to calculate your retirement number:

Write up a detailed monthly budget of your current expenses.

Make adjustments for retirement, including potentially paying off your mortgage or traveling.

Subtract your Social Security benefits and other sources of income from your total expenses.

Multiply by 25 to get your retirement nest egg number.

This calculation uses the 4% withdrawal method. That means that for the first year of retirement, you’ll withdraw 4% of your retirement nest egg. Every year after that, you should adjust for inflation. Some financial planners prefer using a more conservative 3%, while others, like retired financial advisor William Bengen, advocate for 4.5% or 5%.

What the 4% withdrawal rule might look like

Suppose you have a $300,000 retirement nest egg. The 4% rule says that you’ll withdraw $12,000 in your first year of retirement, giving you $1,000 per month, on top of Social Security and other income sources. If inflation in that first year were 2%, you’d multiply $12,000 (your initial withdrawal) by 1.03 to determine your withdrawal for the next year, accounting for inflation. So you’d withdraw $12,360 for year two. And if inflation in year two is 3%, you’d multiply $12,360 by 1.03 and withdraw $12,730.80 for year three.

What to consider

Aside from your savings, other factors that may speed up or delay your retirement include:

Your full retirement age. Since these calculations assume that you’ll receive your full Social Security benefits, you might need to save a bit more if you choose to retire earlier and take Social Security right away.

Debt. If you still have debt payments, you’ll need to account for this expense or push your retirement number.

Other sources of income. Other sources of revenue, including 401(k)s, individual retirement accounts (IRAs), pensions, investment portfolios and Social Security benefits, can reduce the need for a larger nest egg and potentially let you retire earlier.

Changes in current living expenses. Consider how your retirement lifestyle will change, including whether you want to travel more or upgrade to a more luxurious standard of living. If you intend to live it up in retirement, you might need to accelerate your savings or hold off retiring for a few years.

Taxes. Some retirement plans, including 401(k)s and IRAs, may be taxable during withdrawal, which can eat into your income. Be sure to consider your tax liabilities during retirement when determining your take-home income.

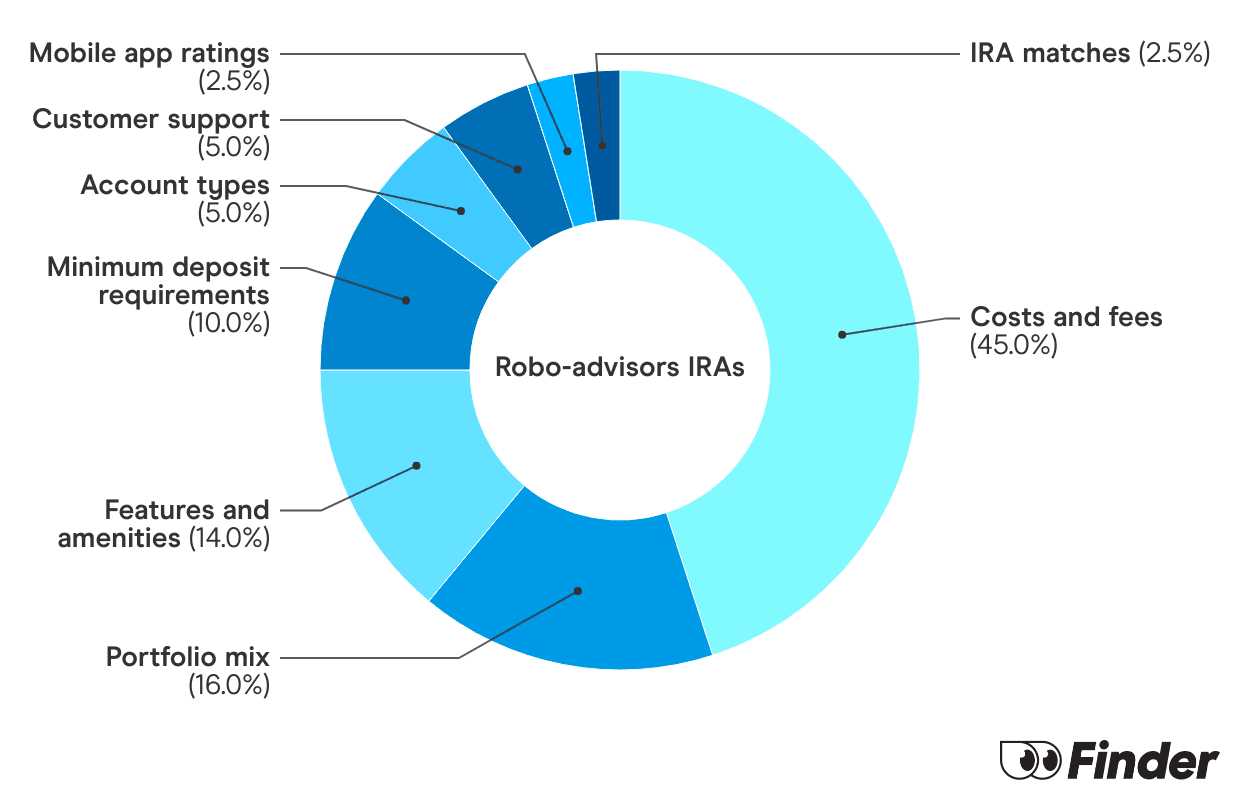

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Bottom line

Calculating your retirement number is a good start for tracking where you are with your retirement goals and how much you’ll need to leave your job. Fortunately, it’s never too late to dive into retirement plans to start saving for the future.

Frequently asked questions

When should I hire a financial planner? You might want to hire a financial advisor when you’re five to 10 years away from retirement. A financial planner can help you:

Stay on track with your retirement goals

Offer advice on growing your investments

Minimize your tax liabilities

Pinpoint when you are ready for retirement

How do I account for inflation in retirement? When you include inflation in your retirement withdrawals, you’d need more money than you did in the previous year. In other words, after your first year of retirement, you should check the average inflation rate of that year and multiply it by your last year’s withdrawal amount. This is the extra amount that you’d need to account for inflation. For example, suppose you withdrew $15,000 for your year one. Since the inflation rate for the last 12 months is about 1.4%, you’d need to add $210 ($15,000 x 0.014) to your initial withdrawal. So your total withdrawal for year two would be $15,210 ($15,000 + $210) after accounting for inflation.

Kimberly Ellis is a personal finance writer at Finder, specializing in banking and financial literacy. After teaching in public and private schools, Kimberly zeroed in on personal financial education to help families and kids develop lifelong money skills. She hails from New York City, graduating summa cum laude from Queens College with a BA in elementary education and mathematics, as well as a New York State teaching certificate. She’s also an aspiring polyglot, always in a book and forever on the hunt for the perfect classic red lipstick. See full bio

Kimberly's expertise

Kimberly has written 85 Finder guides across topics including:

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.