If you’re leaving your current job, you might want to roll over your 401(k) to your new employer’s retirement plan or an individual retirement account (IRA). You may also consider opting for a Roth option if you expect to be in a higher income bracket during retirement. Here’s how to roll over a 401(k).

How do I roll over my 401(k)?

You have several 401(k) rollover options when it comes to transferring your 401(k) from an old job. The process may vary depending on what type of retirement account you choose.

Roll over a 401(k) into another 401(k)

Confirm that your new 401(k) plan accepts 401(k) transfers.

Complete a transfer form with your new plan’s provider, which generally requires your personal information like your Social Security number, your employee info and details about your old 401(k) plan.

Contact your previous employer to see if you need to complete any additional paperwork.

The new and old plan sponsors approve the transfer.

Your old provider issues a check to distribute your 401(k) account balance.

Your new provider deposits the check and purchases investments according to your plan instructions.

Find out whether your new company allows you to roll over your 401(k) directly to a Roth IRA. Otherwise, you may need to roll over your 401(k) funds into a traditional IRA first and then convert it to a Roth IRA.

Fill out a rollover request with your new broker.

Ask your previous employer if there are any forms to fill out on their end.

Both your new and old providers approve the transfer.

If your new brokerage doesn’t allow you to contribute your 401(k) directly to a Roth IRA, your previous plan sponsor will distribute your 401(k) into a traditional IRA.

Open a new Roth IRA.

Fund your Roth IRA using the distribution from your traditional IRA.

Since a Roth IRA is funded with after-tax income, you’ll need to pay income taxes on the amount that you transfer into your Roth IRA.

Borrow from your Beagle 401(k) or IRA with 0% net interest

Robo-advisor available if you roll over your 401(k) to Beagle

Advantages of rolling over a 401(k)

Rolling over your 401(k) has distinct benefits, including consolidating your retirement accounts and potentially avoiding fees your previous plan may charge former employees. Transferring your 401(k) to your new employer’s 401(k) plan lets you continue to fund your plan while deferring taxes until you withdraw from the account. And if you continue working at the same company, you may delay the required minimum distributions (RMD) when you turn 72. Since individual retirement accounts (IRA) are individually owned, rolling over your 401(k) to an IRA means you don’t have to worry about rolling your account over again if you change jobs. And IRAs generally have more investment choices than employer-sponsored 401(k) plans.

Keeping a 401(k) where it is

Employers generally allow you to keep your 401(k) where it is if your account balance is over $5,000. If you’re happy with your current investment options and management fees, you may consider leaving your money where it is. But if you change jobs often, you could end up leaving behind a series of 401(k) plans that could prove challenging to manage. And if you’re no longer working for the company that sponsors the account, you may need to withdraw the required minimum distribution (RMD) from each account every year when you turn 72.

Avoiding penalties and fees when rolling over a 401(k)

There are several ways to avoid incurring taxes and penalties when rolling over a 401(k). When initiating a transfer request, it’s best to request a direct rollover so your old plan administrator can make the payment directly to your new retirement plan or IRA. If your distribution is paid directly to you instead of directly to your new retirement plan or IRA, your employer will withhold 20% of the amount. And you’ll have 60 days to roll it over to another plan and make up the funds for the taxes withheld, or the IRS will treat it as a taxable withdrawal, which may be subject to income tax and early withdrawal penalty if you’re under 59 and a half years old.

Compare retirement accounts

1 - 7 of 7

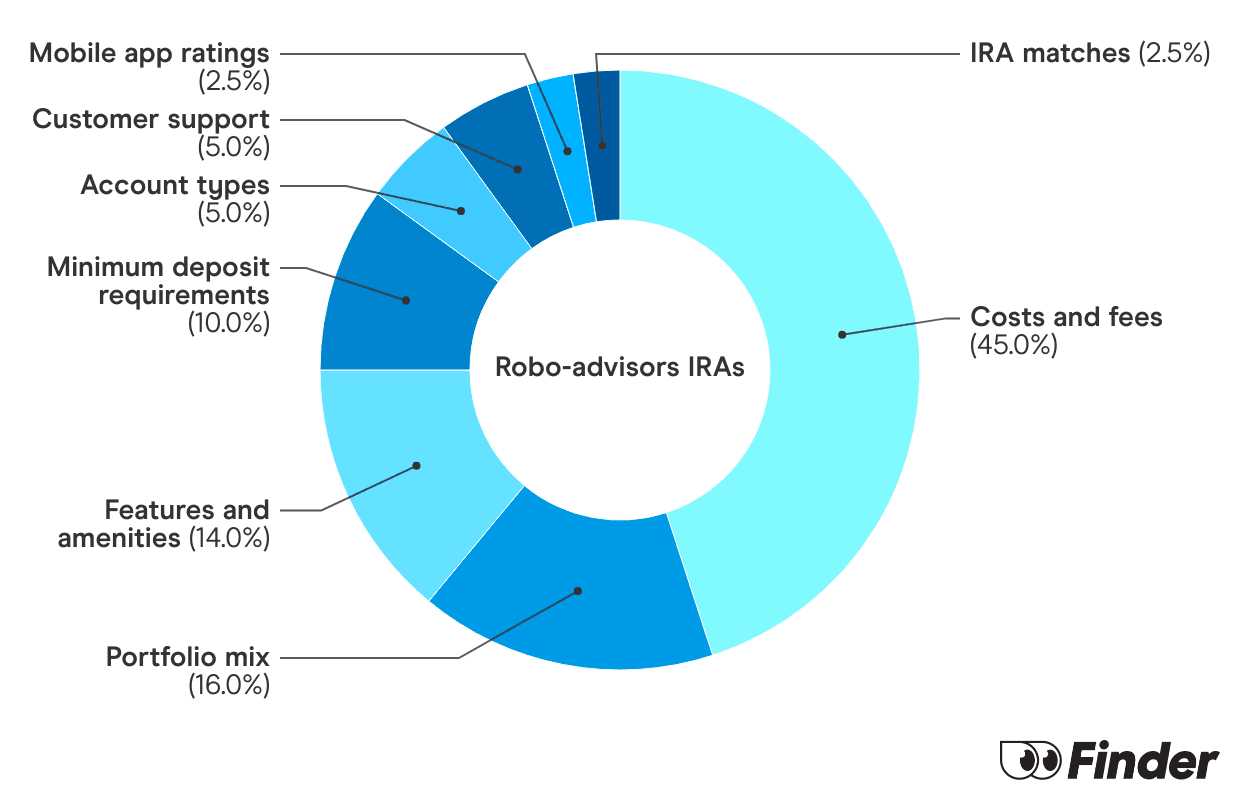

What is the Finder Score?

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

do not lose those balances

How much do you have for retirement?

Response

Contributions

Balance

Amount

$7,409.56

$196,192.48

Source: Finder survey by Qualtrics of 2,033 Americans

With the average adult contributing $7,410 per year to their retirement, it pays to be on the lookout for lost funds. In fact, the average retirement balance currently sits at $196,192.

Bottom line

Be sure to weigh all your options when considering rolling over a 401(k), including tax implications and potential penalties. If your new employer’s 401(k) isn’t a good fit, compare brokerages to find the right IRA for your retirement goals.

Frequently asked questions

If you missed the deadline because of circumstances out of your control, you can apply for a waiver from the IRS.

Roll over a portion of your 401(k) instead of the full amount if your new plan or IRA allows it. If permissible, you can specify how much you want to transfer on the rollover form.

You generally can’t roll over a 401(k) loan unless your company was acquired and you’re employed by the new company.

Kimberly Ellis is a personal finance writer at Finder, specializing in banking and financial literacy. After teaching in public and private schools, Kimberly zeroed in on personal financial education to help families and kids develop lifelong money skills. She hails from New York City, graduating summa cum laude from Queens College with a BA in elementary education and mathematics, as well as a New York State teaching certificate. She’s also an aspiring polyglot, always in a book and forever on the hunt for the perfect classic red lipstick. See full bio

Kimberly's expertise

Kimberly has written 85 Finder guides across topics including:

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.