Finder maintains full editorial independence to ensure for our readers a fair assessment of the products, brands, and services we write about. That independence helps us maintain our reader's trust, which is what keeps you coming back to our site. We uphold a rigorous editorial process that ensures what we write and publish is fair, accurate, and trustworthy — and not influenced by how we make money.

We're committed to empowering our readers to make sound and often unfamiliar financial decisions.

We break down and digest information information about a topic, product, brand or service to help our readers find what they're looking for — whether that's saving money, getting better rewards or simply learning something new — and cover any questions you might not have even thought of yet. We do this by leading with empathy, leaning on plain and conversational language that speaks directly, without speaking down.

Do you dream of escaping the hustle and bustle of your work life? You may have heard about early retirement but have never taken the time to see if it’s an option for you.

To retire early, you have to balance your lifestyle expectations with your savings, investments and expenses.

Access a team of fiduciary portfolio management specialists and financial, tax and estate planning professionals.

Transparent fee structure with no commission-based products.

Get tax-efficient wealth management that reduces your tax burden and preserves more of your assets.

Tailored financial plans for your unique needs and goals.

Ongoing consultations to adapt your evolving plan.

How to retire early in 5 steps

Early retirement is no easy task. It takes planning, commitment and discipline. And it will likely require you to make financial sacrifices today so you can leave the workforce ahead of schedule.

Here are five steps to take to put yourself in a position to potentially retire early.

1. Choose an early retirement age

The first step in retiring early is to ignore the general noise around when most people retire and figure out what “retiring early” means to you. For instance, the regular retirement age according to the U.S. Social Security Administration is 67. However, you may choose to retire early depending on how much you have saved.

“It’s important to note that there is no single number of assets dedicated for retirement that fits everyone,” says Giovanni Valle, CFP®, Financial Planner at Avantax. “I’ve seen people be completely fine retiring with Social Security income and no assets and others need a million [or] $5 million, all depending on the lifestyle you’re comfortable living during retirement.”

Decide when you’d like to retire so you have a concrete time frame.

How to retire at 40

According to 2022 data by Gallup, Inc., only 3% of retired Americans were ages 40 to 49. While rare, Valle has some tips for those who have such ambitious goals.

“My advice for someone wanting to retire by 40 is to recognize that you will likely have to make trade-offs in your current lifestyle, including saving at least 50% of your income and figuring out ways to earn more income,” Valle says. “Know the basics of limits regarding different types of accounts such as various retirement accounts, taxable investment accounts, or HSA accounts.”

Be mindful of early withdrawal penalties

If you withdraw funds from an individual retirement account (IRA) before the age of 59 and a half, you will likely incur a 10% early withdrawal penalty. Roth IRA earnings face the same penalty for early withdrawals, but Roth IRA contributions are available for withdrawal at any time penalty- and tax-free.

How to retire at 55

From 2016 to 2022, only 6% of Americans between the ages of 50 and 54 were retired, according to the same Gallup study. This percentage shows that even if in an older range, retiring “early” is still rare.

Valle does caution that since 55 is still a bit younger than the traditional retirement age, saving at least 25% of your income can help better position yourself for early retirement.

Once you reach age 55, know what resources are available to fund your retirement.

“My advice for someone wanting to retire at 55 is to be aware of the rule of 55,” Valle says. “This rule allows penalty-free withdrawals from a 401(k) and 403(b) account with your current employer if you leave your job the calendar year you turn 55 or later, including if you get laid off or quit your job.”

It’s worth noting that longer life expectancies will contribute to a need to save longer. According to the Centers for Disease Control and Prevention (CDC), the current life expectancy is around 76 years old. As it has over the years, life expectancies may change. Valle recommends keeping a 30-year time horizon in mind.

2. Calculate your retirement expenses

When preparing for retirement, it’s important to know how much you need saved to support your preferred lifestyle. The Spending in Retirement Survey by the Employee Benefit Research Institute (EBRI) shows how retirees typically spend their money.

The survey revealed that housing is the largest reported expenditure for retirees, followed by food, transportation and then medical and health insurance.

Housing. Housing expenses can include mortgage payments, property taxes, home insurance, ongoing maintenance costs and more. A recent survey by Clever Real Estate highlighted that 24% of retirees were carrying housing-related debt as of November 2022.

Food. Food costs come in a close second to housing expenses in the ERBI study — 26% of respondents said their second largest monthly expense in retirement is food. This includes groceries and dining out.

Travel Expenses. Budgeting for leisure travel and vacations is another important aspect of retirement planning that you should consider when planning to retire early. About 36% of retirees reported that their overall spending, which included travel-related expenses, was higher than expected.

Health Insurance. Health insurance premiums, copays and potential long-term care costs make up a huge portion of retirees’ spending, according to the EBRI study. According to the EBRI, a couple would need $296,000 saved to have a 90% chance of meeting all healthcare expenses.

3. Estimate how much you’ll need to retire

The amount you need to retire depends on several factors, including your retirement length and lifestyle. However, there are three common rules of thumb to estimate how much you need in your post-work years.

One is “The 4% Rule.” This rule states that retirees should aim to withdraw 4% of their retirement savings each year to maintain enough in their savings to last a 30-year retirement. Estimate how much money you’ll need each year to cover your expenses and live comfortably, and calculate how much is 4%. For example, if you need $75,000 a year in retirement, you might aim to save $1,875,000 ($75,000 is 4% of $1,875,000). This rule assumes a portfolio with a healthy mix of stocks and bonds.

Another rule to consider is “The 80% Rule,” which states that you should have enough saved to replace 80% of your pre-retirement amount. This rule is based on the assumption that while work-related costs may decrease in retirement, healthcare and leisure activities may rise.

Lastly, a third rule you may hear in retirement circles is “The Rule of 25,” which is based on your annual expenses. Find out how much you’d need to withdraw each year to cover your expenses. Then, multiply this amount by 25. Let’s say you’d like to withdraw $20,000 a year in retirement. This means you need $500,000 saved up for your golden years.

Use your investment calculator to determine how much your money might grow and return over time, based on contribution frequency, rate of return and time horizon.

4. Create a retirement plan to get there

After you have an age set for when you want to retire and an estimated savings amount needed, here are a few other factors you should consider in your retirement planning.

The first is your current financial situation. Even if you have a retirement amount in mind — let’s say $1 million — you may currently have additional debts you have to pay, such as education or mortgages. Consider the time it will take to pay off these debts in your retirement equations. To expedite the debt-repayment process, you may explore a second job or additional income streams.

The next is to keep a careful eye on your budget. The 2022 Employee Benefit Research survey stated that 27% of retirees spend more than they can afford. So, even if you reach your retirement-saving goal, not sticking to a budget can derail your efforts.

Last but not least, explore taking advantage of tax-advantaged retirement accounts to meet your retirement number. This could mean working towards maxing out your IRA and contributing at least enough in a 401(k) to get any company match since that’s essentially free money from your employer. These accounts have tax advantages that you can tap into.

As of 2024, the following annual contribution maximums for tax-advantaged accounts are:

401(k): $23,000

IRAs: $7,000

Health savings account (HSA): $4,150 (self) and $8,300 (family coverage)

It’s important to regularly review your retirement plan to make sure it still fits your needs. Consider reassessing it at least once a year or during significant life changes. This will help you make any necessary adjustments to ensure you’re on track for a comfortable retirement.

What’s the earliest age to retire?

You can retire at any age you choose, but you may receive Social Security retirement benefits beginning only at the age of 62. If you opt for these benefits before your full retirement age, your benefits will be reduced. The full retirement age varies based on your birth year, typically ranging from 66 to 67.

Compare brokerages that offer IRA accounts

Compare IRA brokers by retirement account types and annual fee. Select Go to site to sign up for an account.

7 of 7 results

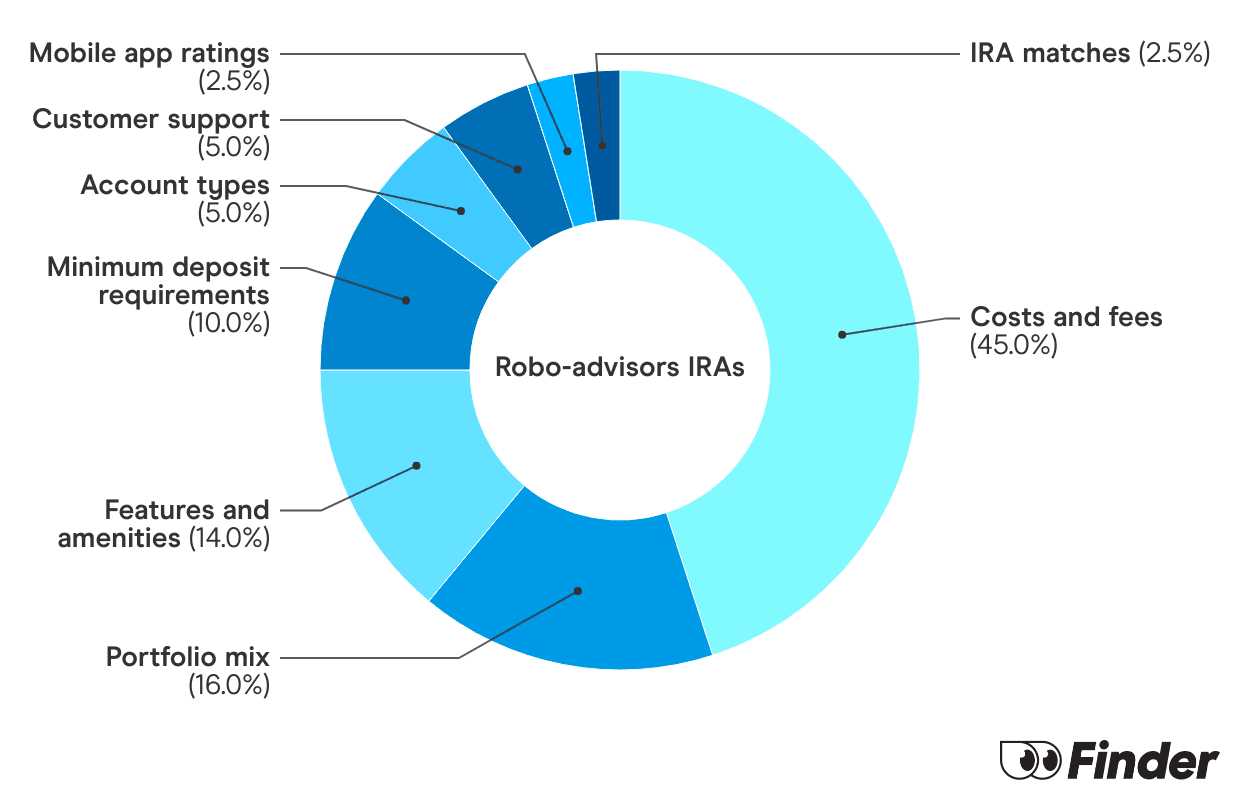

What is the Finder Score?

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Bottom line

At the end of the day, early retirement is a dream that is attainable if you have the right combination of savings, assets and Social Security benefits to support your lifestyle and life horizon. To learn more about how to plan for retirement, explore our retirement education and tools.

Frequently asked questions

According to experts, the common way to retire early is to take advantage of tax-efficient retirement accounts such as a 401(k), Roth IRA and regular IRA early on. If you have an employer match program, you may want to consider taking advantage of that as well as saving and investing. This, in addition to knowing how much money you need to retire, can help you retire early.

There is no universal "good age" for retirement. The right age is subjective and depends on your unique goals.

As a rule of thumb, Fidelity states you should have at least 1x your salary saved by 30, 3x by 40, 6x by 50, 8x by 60 and 10x by 67.

This depends on your retirement lifestyle. If the average life expectancy is 74 years, then you'll have to make that $1 million last hypothetically 19 years — age 55 to 74 — which gives you a budget of about $52,000 per year.

While it's tough to retire without savings of your own, you may want to ask your financial planner to see how you can maximize your Social Security benefits and if there's a possibility to claim them early.

Dhara Singh was a freelance personal finance writer at Finder specializing in loans. Formerly she was a top 10 journalist at Yahoo Finance with more than 38+ million content views where she covered retirement and mortgages. She has also written for Bankrate, and CNET and continues to write for a variety of outlets, such as Investopedia and Worth magazine. Her articles focus on equipping readers with the right information and data so they can make the most informed decisions related to their finances.

Dhara previously worked as an insights analyst for Finder’s PR team, where she started the Deadliest Cities to Drive series in 2018, connecting interesting data analysis to a suite of car insurance products. When she’s not writing, Dhara coaches small business owners through her Stories to Sales programs and empowers them to use their life experiences to help other people. She has also self-published a poetry book on Amazon called Tell her She’s Lovely.

Dhara holds a B.S. in Finance and Supply Chain Management from Rutgers University and a M.S. in Journalism from Columbia University.

See full bio

Here’s how retirement savings accounts work and how to compare your options.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.