If you’ve been living in your home for a while, chances are you’ve built up equity in your home. The beauty of home equity is that you can tap into it with a home equity loan or cash it out when you sell your house. Here’s a closer look at what home equity is, how to calculate it and how to increase it with some smart financial strategies.

Key takeaways

Home equity is the difference between your home’s current market value and what you still owe on it — including your mortgage balance and any other secured debts like a home equity loan or HELOC.

Equity grows in two ways: by paying down your mortgage principal and through your home appreciating in value. A $300,000 home bought with a 20% down payment starts with $60,000 in equity — but five years of payments and market appreciation can push that significantly higher.

You can access your equity in three main ways: a home equity loan (lump sum at a fixed rate), a HELOC (flexible revolving credit line), or a cash-out refinance (replacing your existing mortgage with a larger one).

The smartest uses of home equity are ones that improve your financial position — paying off high-interest debt, funding home improvements or making a down payment on an investment property. Using it for discretionary spending like vacations is generally not advisable.

The five-year rule is worth following: staying in your home for at least five years gives you the best chance of selling for more than you paid and recouping your closing costs.

This summary was generated by AI and may contain errors or omissions.

Home equity definition

Home equity is the difference between your current mortgage balance (plus any other debts against your home) and your home’s current market value. You can calculate your home equity if you know these numbers:

Current market value. This is what your home should sell for in the current market as determined by a qualified home appraiser.

Mortgage balance. This is the outstanding balance on your current mortgage. Your mortgage balance is listed on your monthly loan statement.

Debts against your home. This might include a home equity loan or home equity line of credit (HELOCs) that you’ve taken out against your property.

If you’re wondering about your home’s worth, a qualified real estate appraiser can give you an estimate. But ultimately, your home is worth what a buyer is willing to pay for it — it could be more or less than the appraised value.

Why does home equity matter?

Home equity is historically one of the best ways of accumulating wealth, and statistics back this up. The typical profit on a home in the US in 2022 is $94,000 – up 71% over pre-pandemic sales prices, according to data from CNBC. And for homes in hot property markets like Florida, Texas and Idaho — home equity and sales profits have been rising even faster.

How home equity works: an example

Suppose you buy a home for $300,000. You put 20% down ($60,000) and get a mortgage for $240,000 to cover the rest. At closing, you have $60,000 worth of equity in your home.

Now, let’s say it’s five years later and you’ve paid down $23,000 of your loan’s principal and the value of your home has appreciated by $50,000. You now have $133,000 worth of equity in your home.

$60,000 down payment

$23,000 in principal payments

$50,000 in appreciation

Total equity: $133,000

7 tips for building equity in your home

While home equity typically takes years to build, here are seven steps you can take to build the equity in your home faster.

Prioritize mortgage payments. Increase your repayment schedule to bimonthly or even weekly payments. Although you’re paying the same amount every month, these extra payments can shave thousands of dollars off your interest so more money goes towards your principal.

Stay in your home for at least five years. This five-year rule helps ensure that you can sell the home for more than you paid for it and recoup your closing costs.

Invest in home improvements. The right improvements — like remodeling an outdated kitchen or bathroom — can help increase your home’s value. Compare home improvement loans to see if it’s the right time to update your home.

Make extra payments toward your principal. Use windfalls and work bonuses to pay down your principal. The more you put towards your principal balance, the faster you’ll increase your equity and reduce your total interest paid at the same time.

Refinance your mortgage. Not only can refinancing help you secure a lower rate, you also refinance to shorten your loan term, which means you’re paying more towards your principal every month and building equity faster.

Get rid of private mortgage insurance (PMI). Once your home equity reaches 20%, you’re allowed to get rid of your PMI. Depending on the type of loan you have, you can ask your lender to remove it or you may have to refinance the loan. The monthly savings can be used to pay down your principal and build your equity.

Wait for your home to increase in value. Another strategy is to live in your home and wait for it to appreciate in value. According to data from CoreLogic, homes in the US are expected to appreciate by 5.6% year-over-year from April 2022 to April 2023.

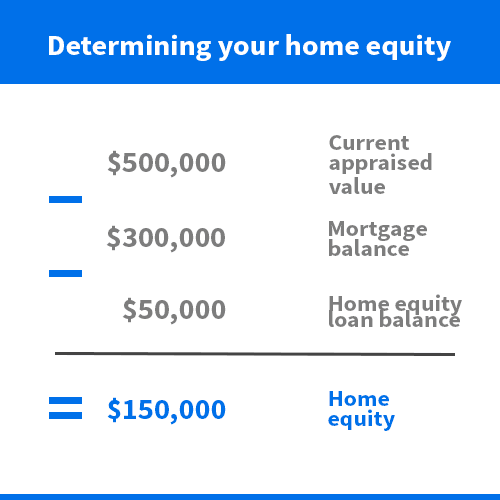

How to calculate home equity

To calculate your home equity, subtract what you owe on all secured debt against your home — including your mortgage and home equity loans, if any — from its current market value.

For example:

Home’s current value: $500,000

Mortgage balance: $300,000

Home equity loan balance: $50,000

Total home equity: $150,000

For more information on the benefits to calculating your home equity, see our guide on how to calculate home equity.

How to use home equity

There are a few ways to use your home equity: get a home equity loan or HELOC, or do a cash-out refinance.

Some common reasons people use home equity include:

To consolidate high-interest debt with a home equity loan or HELOC.

To make home improvements with a home equity loan or HELOC.

To make a down payment on an investment or vacation property.

To take out a reverse mortgage during retirement.

To do a cash-out refinance and secure a lower interest rate at the same time.

Because you’re taking on more debt with these methods, it’s advisable to only use the money in a way that makes financial sense. For example, using home equity to fund a luxury vacation is probably not a good use of your home’s value. On the other hand, using home equity to pay off high-interest student loan debt can be a smart financial move.

HELOCs and home equity loans each have their pros and cons and are used for different purposes. To learn more, see our guide on home equity loans vs. HELOCs.

Compare interest rates for home equity loans, HELOCs and cash-out refinancing

Use our tool to get personalized estimated rates from top lenders based on your location and financial details. Select whether you’re looking for a Home Equity Loan, HELOC or Cash-Out Refinance.

If you selected a home equity loan or HELOC, enter your ZIP code, credit score and information about your current home to see your personalized rates.

In the Cash-Out Refinance tab, select Refinance and enter your ZIP code, credit score and other property details to see what you might qualify for.

Searching for the best rates...

Bottom line

Home equity is wealth you can tap into while you own your home and profit from when you sell your home. If now is the right time to access your home equity, compare HELOC rates and lenders or learn more about how home equity loans work.

Kat Aoki was a personal finance writer at Finder, specializing in consumer and business lending. She’s written thousands of articles to help consumers make better decisions on their home loans, bank accounts, credit cards, cryptocurrency and more. Kat is well versed in working with leading brands in the real estate, mortgage and personal finance industries, and her expertise has been featured on Lifewire and financial comparison sites like iSelect and realestate.com.au. She holds a BS in business administration from California State University, Sacramento and enjoys hiking and yoga in her spare time.

See full bio

Kat's expertise

Kat

has written

132

Finder guides across topics including:

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.