Finder makes money from featured partners, but editorial opinions are our own.

Advertiser disclosure

1% IRA Match

- $0 annual fee and no stock or ETF commissions

- Robo-advisor and financial planning sessions

- Access private credit, venture capital and other alternative asset funds

- Get a 1% IRA Match on contributions and rollovers

Terms and conditions apply*. For 401k rollovers, existing SoFi IRA members must complete 401k rollovers via this link For SoFi members without a SoFi IRA, a SoFi IRA must first be opened, and 401k rollover must be completed utilizing Capitalize via this link. SoFi and Capitalize will charge no additional fees to process a 401(k) rollover to a SoFi IRA. SoFi is not liable for any costs incurred from the existing 401k provider for rollover. Please check with your 401k provider for any fees or costs associated with the rollover. For IRA contributions, only deposits made via ACH and cash transfer from SoFi Bank accounts are eligible for the match. Click here for the 1% Match terms and conditions.

Must be a SoFi Plus member at the time a recurring deposit is received into your SoFi Active or Automated investing account to qualify. Bonus calculated on net monthly recurring deposits made via ACH and paid out as Rewards Points. See Rewards Terms of Service. SoFi reserves the right to change or terminate this promotion at any time without notice. See terms and limitations. https://www.sofi.com/sofiplus/invest/#disclaimers

Must be a SoFi Plus member at the time a recurring deposit is received into your SoFi Active or Automated investing account to qualify. Bonus calculated on net monthly recurring deposits made via ACH and paid out as Rewards Points. See Rewards Terms of Service. SoFi reserves the right to change or terminate this promotion at any time without notice. See terms and limitations. https://www.sofi.com/sofiplus/invest/#disclaimers

1%–3% match

- Get 1%–3% match on contributions, IRA transfers and 401(k) rollovers

- Choose your investments or get a recommended portfolio of ETFs

- Get bigger instant deposits, professional research and more with Robinhood Gold

Best Rollover IRA accounts

We’ve curated 4 standout platforms to help you find the best IRA accounts for an IRA rollover.

- Acorns: Best for investing small amounts

- M1 Finance: Best for hybrid investors

Robinhood Retirement

8.8 Great

- Best for investors looking for a platform to partially match their Roth IRA contributions Robinhood contributes up to 3% for every dollar you invest into your Roth IRA on its platform.

Robinhood offers commission-free trades and zero management fees for its Roth IRA product.

And not only does Robinhood not charge fees, but it actually gives you money when you invest in your Roth IRA on the platform. If you max out your IRA contributions for 2024 and stack on your max contributions for 2025 by April 15, Robinhood matches 3% for Gold subscribers and 1% without, for a bonus of up to $420.

It's worth noting, though, that you can only invest in stocks and ETFs via Robinhood's Roth IRA. Your investments on the platform are protected up to $500k, as Robinhood is a member of SIPC (Securities Investor Protection Corporation).

Also, keep in mind that the platform's customer support is lacking as compared to bigger platforms like Fidelity or Charles Schwab. So, if you're looking for some one-to-one help as you build your nest egg, Robinhood might not be the best choice for you.

| Annual fee | $0 per month |

|---|---|

| Minimum deposit | $0 |

| Signup bonus | Earn up to a 3% match with Robinhood Gold or 1% without |

| Annual fee | $0 per month |

|---|---|

| Minimum deposit | $0 |

| Signup bonus | Earn up to a 3% match with Robinhood Gold or 1% without |

SoFi IRA

8.4 Great

- For investors who want guidance. SoFi offers no-fee automated investing and personalized financial advice from a licensed human investment advisor at no additional cost.

SoFi offers some of the most competitive pricing on our list. In addition to no-fee commission stocks and exchange-traded funds (ETFs), it offers no-fee account transfers and its robo-advisor charges a small 0.25% annual fee. For those who want access to a human advisor, SoFi's licensed investment specialists are standing by. This feature makes SoFi a practical fit for both hands-on and hands-off retirement-focused investors. Whether you're keen to buy and sell your own securities or let an algorithm do it for you, SoFi's active and automated Roth IRAs may fit the bill.

This brokerage is a practical fit for new traders seeking access to stocks and ETFs. Mobile app reviews suggest that the platform is intuitive and receives high praise from both Apple and Android users.

SoFi's major drawback is its limited asset offerings. While you can invest in stocks and ETFs in your Roth IRA via SoFi, you cannot invest in cryptocurrencies in it.

| Annual fee | $0 per month |

|---|---|

| Minimum deposit | $0 |

| Annual fee | $0 per month |

|---|---|

| Minimum deposit | $0 |

Acorns Later

8.4 Great

- Best for investing small amounts Acorns rounds-up your debit or credit card purchases to the nearest dollar and enables you to invest the difference.

Acorns Later is the name of the division of Acorns that allows you to invest for your retirement. One of the products that Acorns Later offers is a Roth IRA, which allows you to save for your retirement with automatic round-ups on purchases.

Through Acorns Later, you can get exposure to stocks, ETFs, bonds, REITs and even a Bitcoin-linked ETF.

Keep in mind, though, that the platform charges a $6 monthly maintenance fee for this account, while a number of other platforms that offer Roth IRAs don’t charge such a fee. With that said, Acorns doesn’t charge any fees for trades.

And you might find the $5 fee worth it, as Acorns Later will automatically adjust your Roth IRA portfolio weighting depending on your age, investment goals and risk tolerance.

| Annual fee | $3 per month |

|---|---|

| Minimum deposit | $0 |

| Signup bonus | N/A |

| Annual fee | $3 per month |

|---|---|

| Minimum deposit | $0 |

| Signup bonus | N/A |

M1 Finance IRA

- Best for hybrid investors. M1’s automation and manual order capabilities makes it suitable for investors who want the option to set it and forget it or take the reins and manage their own portfolio.

M1 Finance is one of the more unique robo-advisors on the market. It offers automated portfolio rebalancing, yes — but it also allows investors to select their own portfolio holdings.

When you sign up for an M1 Finance Roth IRA, it prompts you to pick at least three investment slices to begin building your portfolio – or your “pie” as M1 likes to call it. It also asks to give each allocation an assigned weight, so M1 Finance knows how to prioritize your selections.

After that, M1 Finance is responsible for automatically rebalancing your portfolio and runs much like a traditional robo-advisor. M1 will only rebalance your portfolio using trades with new cash. It won’t sell an existing position or initiate a rebalance of your portfolio without your instruction.

You need at least $500 to get started, and there's no annual management fee. But M1 Finance doesn't offer true self-directed trading accounts, so active traders will need to look elsewhere.

| Annual fee | $0 per month |

|---|---|

| Minimum deposit | $500 |

| Signup bonus | N/A |

| Annual fee | $0 per month |

|---|---|

| Minimum deposit | $500 |

| Signup bonus | N/A |

How we picked these platforms

We took a close look at platform features, fees, account minimums, customer support, research tools and mobile apps to curate this list of best Roth IRA accounts. Our honorable mentions went to platforms with less competitive fees but that had a niche feature or perk not typically found across traditional brokerages.

How do I roll over my 401(k)?

If you’re leaving your current job, you might want to roll over your 401(k) to your new employer’s retirement plan or an individual retirement account (IRA). You may also consider opting for a Roth option if you expect to be in a higher income bracket during retirement.

Here’s how to roll over a 401(k).

You have several 401(k) rollover options when it comes to transferring your 401(k) from an old job. The process may vary depending on what type of retirement account you choose.

Roll over a 401(k) into another 401(k)

- Confirm that your new 401(k) plan accepts 401(k) transfers.

- Complete a transfer form with your new plan’s provider, which generally requires your personal information like your Social Security number, your employee info and details about your old 401(k) plan.

- Contact your previous employer to see if you need to complete any additional paperwork.

- The new and old plan sponsors approve the transfer.

- Your old provider issues a check to distribute your 401(k) account balance.

- Your new provider deposits the check and purchases investments according to your plan instructions.

Roll over a 401(k) into a Roth IRA

- Compare and pick your new Roth IRA provider.

- Find out whether your new company allows you to roll over your 401(k) directly to a Roth IRA. Otherwise, you may need to roll over your 401(k) funds into a traditional IRA first and then convert it to a Roth IRA.

- Fill out a rollover request with your new broker.

- Ask your previous employer if there are any forms to fill out on their end.

- Both your new and old providers approve the transfer.

- If your new brokerage doesn’t allow you to contribute your 401(k) directly to a Roth IRA, your previous plan sponsor will distribute your 401(k) into a traditional IRA.

- Open a new Roth IRA.

- Fund your Roth IRA using the distribution from your traditional IRA.

- Since a Roth IRA is funded with after-tax income, you’ll need to pay income taxes on the amount that you transfer into your Roth IRA.

Roll over a 401(k) into a traditional IRA

- Compare and select a new brokerage for your IRA.

- Submit a rollover form with your new company.

- Complete any additional documents your previous plan’s provider may require.

- Your old and new sponsors approve the rollover.

- Your current financial company issues a check to your new IRA provider.

- Your new IRA company deposits the check into your account.

Roll over a Roth 401(k) into a new 401(k)

If you currently have a Roth 401(k), you must transfer the funds to another Roth account.

Roll over a Roth 401(k) into a new Roth 401(k)

- Verify that your new employer offers Roth 401(k) retirement accounts and allows transfers.

- Complete a transfer form with your new employer’s Roth 401(k) sponsor.

- Reach out to your old company about its rollover process, including any additional paperwork you may need to fill out.

- Both your old and new employers approve the transfer.

- Your old plan’s Roth 401(k) provider issues a check to your new company.

- Your new Roth 401(k) company funds your account with the check.

Advantages of rolling over a 401(k)

Rolling over your 401(k) has distinct benefits, including consolidating your retirement accounts and potentially avoiding fees your previous plan may charge former employees.

Transferring your 401(k) to your new employer’s 401(k) plan lets you continue to fund your plan while deferring taxes until you withdraw from the account. And if you continue working at the same company, you may delay the required minimum distributions (RMD) when you turn 73.

Since individual retirement accounts (IRA) are individually owned, rolling over your 401(k) to an IRA means you don’t have to worry about rolling your account over again if you change jobs. And IRAs generally have more investment choices than employer-sponsored 401(k) plans.

Keeping a 401(k) where it is

Employers generally allow you to keep your 401(k) where it is if your account balance is over $5,000. If you’re happy with your current investment options and management fees, you may consider leaving your money where it is.

But if you change jobs often, you could end up leaving behind a series of 401(k) plans that could prove challenging to manage. And if you’re no longer working for the company that sponsors the account, you may need to withdraw the required minimum distribution (RMD) from each account every year when you turn 73.

Avoiding penalties and fees when rolling over a 401(k)

There are several ways to avoid incurring taxes and penalties when rolling over a 401(k). When initiating a transfer request, it’s best to request a direct rollover so your old plan administrator can make the payment directly to your new retirement plan or IRA.

If your distribution is paid directly to you instead of directly to your new retirement plan or IRA, your employer will withhold 20% of the amount. And you’ll have 60 days to roll it over to another plan and make up the funds for the taxes withheld, or the IRS will treat it as a taxable withdrawal, which may be subject to income tax and early withdrawal penalty if you’re under 59 and a half years old.

Compare brokerages that offer Rollover IRA accounts

4 of 4 results

What is the Finder Score?

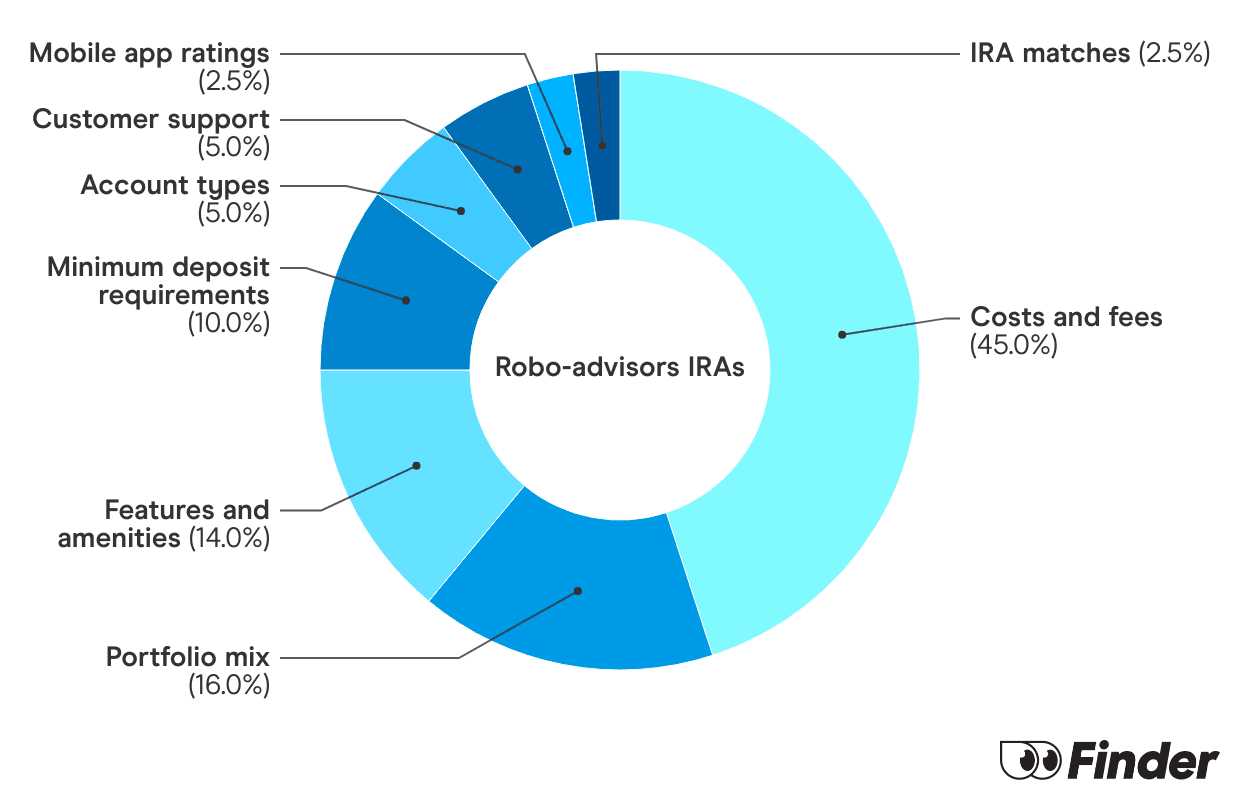

The Finder Score crunches 147 key metrics we collected directly from 18+ brokers and assessed each provider’s performance based on nine different categories, weighing each metric based on the expertise and insights of Finder’s investment experts. We then scored and ranked each provider to determine the best brokerage accounts.

We update our best picks as products change, disappear or emerge in the market. We also regularly review and revise our selections to ensure our best provider lists reflect the most competitive available.

What different scores mean

9+

Excellent

These are the online brokers that offer the lowest fees coupled with plenty of trading options, account types and other features, giving the best overall value.

7+

Great

These brokers may have fewer investment options, slightly higher fees, might lack a browser platform, or don’t offer 24/7 customer service, but overall, a competitive offering.

5+

Standard

Usually, these brokers still offer above-average investment options and account types and may include some competitive features, but they're not the best value for the overall cost.

0+

Basic

These brokers have a small number of investment options, high fees, poor mobile app ratings and/or limited methods for contacting customer service.

Paid non-client promotion. Finder does not invest money with providers on this page. If a brand is a referral partner, we're paid when you click or tap through to, open an account with or provide your contact information to the provider. Partnerships are not a recommendation for you to invest with any one company. Learn more about how we make money.

Finder is not an advisor or brokerage service. Information on this page is for educational purposes only and not a recommendation to invest with any one company, trade specific stocks or fund specific investments. All editorial opinions are our own.

Bottom line

Be sure to weigh all your options when considering rolling over a 401(k), including tax implications and potential penalties. If your new employer’s 401(k) isn’t a good fit, compare brokerages to find the right IRA for your retirement goals.

Frequently asked questions

Ask a question

Read more on Retirement

-

Top IRA Match Accounts for 2026: Boost Your Retirement Today

Get up to a 3% IRA match with Robinhood and Acorns or a 1% IRA match with Public. See how to qualify here.

-

5 Best SEP IRA Providers of 2026

Explore the pros and cons of the best SEP IRAs and learn how to open one of these accounts.

-

What Is a Sep IRA and How Does It Work?

What you need to know about SEP IRAs and how these retirement accounts work.

-

What Is a Traditional IRA and How to Open One

Learn about what traditional IRAs are and how they work.

-

10 Best Roth IRAs for 2026: Top Retirement Picks

Check out the best Roth IRA providers overall — with guidance on which ones tend to work best for different investing styles.

-

10 Best IRAs for 2026: Top Retirement Picks

Check out the best IRA providers overall — with guidance on which ones tend to work best for different investing styles.

-

Should I Max Out My 401(K)?

The rush of turning $19,500 into $1 million can be enticing, but it’s not always the best idea.

-

Roth IRA vs. Traditional IRA: What’s the Difference?

Learn the differences between a Roth IRA and a traditional IRA.

-

What is a Roth IRA and how to open one

Learn how Roth IRAs work and who qualifies to open one.

-

What Is a Retirement Savings Account?

Here’s how retirement savings accounts work and how to compare your options.