Business loan cost comparison

Loan amount: £50,000

- Loan term: 1 year

- Interest rate: 22%

- Monthly repayment: £4,633

- Total interest: £5,595

Loan amount: £50,000

- Loan term: 1 year

- Interest rate: 36%

- Monthly repayment: £4,903

- Total interest: £8,831

A short term business loan can help smooth out your company's cash flow or cover the cost of upcoming purchases. Use the table below to compare competitive business loans from a range of lenders, based on loan types, amounts and terms, and eligibility criteria.

To make comparing even easier we came up with the Finder Score. Costs, speeds and features across 50+ lenders are all weighted and scaled to produce a score out of 10. The higher the score the better the lender – simple.

Read the full methodologyA short term business loan is one of the most common ways to help manage cashflow, finance a new startup and help scale a successful businesses.

However, the difference between securing the best and worst terms on a short term loan could make a substantial difference to a business’s bottom line.

In this guide, you’ll learn whether a short term loan is right for your business, how to find the best deal and how the approval process typically works.

Business owners may take out a short term loan when they require additional funds to cover an upcoming purchase or large expense, or when their business is facing a temporary cash flow issue. Generally speaking, business loans with a term less than 18 months or 2 years are considered short term and can even come with daily or weekly repayments instead of monthly repayments.

Short term business loans will normally fit within the following criteria:

In all cases, the lender will consider your business credit score, annual turnover and how long you’ve been in business during the approval process. In many cases, it will display minimum eligibility criteria for all three of these factors.

In many cases, you can apply for a short term business loan very quickly online using the lender’s website.

You’ll need to fill in a few essential personal details as well as the essential details to identify your business, such as your company type, business address and limited company number.

In most cases, you’ll also need to provide financial details and proof of income, such as VAT returns and bank statements. You may also need to explain why you’re applying for a loan.

Some lenders will make an instant decision on your application. Others take two to three business days. Once your loan has been approved, you can sometimes expect to be credited with your loan on the same business day.

Lenders use a business credit score to assess the creditworthiness of your business.

Credit reference agencies calculate your business credit score based on information in your business credit file. The factors they use to measure your score include borrowing history, previous credit applications, current debt, debt payment history and the number of years the company has been in business.

Different lenders will use different credit reference agencies to measure your business credit score. Your score will determine the terms of the loan offered to you, if you’re considered eligible at all.

To ensure your business maintains a healthy credit score, don’t open too many lines of credit or push your existing lines too close to their limit. This makes your business appear as a risky prospect. However, it’s generally worth opening some lines of credit and making timely repayments in order to build your company’s credit score.

Short term business loans are a handy option if you’re looking to borrow large sums of money with short notice, but they’re not always the best option.

A business credit card could prove more useful if you’re looking to cover immediate expenses. Although the maximum borrowing amount doesn’t tend to be as high, the application process typically isn’t as strict or as complicated as applying for a short term loan. It’s possible to attach multiple cards to the same account, which can prove to be a useful way to manage employee spending.

It may also be possible to add an overdraft onto your current business account, which will give you access to additional funds as and when you need them. Often, the lender will agree to leave an overdraft in place for a fixed amount of time before removing it.

If it’s unlikely your business will be able to repay the loan over two years or less, consider a medium or long term business loan instead. The repayments on these longer deals will be lower, although you’ll pay more interest in total.

There’s no one-size-fits-all business loan. The loan type that works best for you depends on your business’s immediate needs and how it operates. Have a lot of outstanding invoices? Invoice factoring might be what you’re looking for. Have an unpredictable and irregular cash flow? Consider a line of credit. Here are some of your options:

These business loans come in one lump sum that you pay back over a set period of time with interest (usually fixed) and fees.

Invoice factoring involves selling your business’s unpaid invoices to a third party for a percentage of their value. Your lender gives your business a smaller percentage of the invoices upfront after deducting a fee. Once your customers pay off the invoices, the lender gives your business the remaining amount.

You can either sign up for monthly invoice factoring to make sure all of your business expenses are covered or use invoice factoring to cover a one-time payment. You can also either factor all of your business’s invoices or select which invoices to factor.

Similar to invoice factoring, invoice financing gives you an advance on your invoices. It’s essentially a loan backed by your company’s invoices. You’ll get a percentage of your invoice value upfront, which you pay back with interest and fees. Once the client pays you, you repay your lender.

Lines of credit give your business access to a certain amount of funds at the last minute, similar to a credit card. You only have to repay what you borrow and your loan term typically starts when you make your first withdrawal. Short term lines of credit typically come with terms that range from 6 to 12 months with weekly or even monthly repayments.

Merchant cash advances are quick lump-sum advances on your business’s future sales. Your business can typically qualify for a certain percentage of its annual sales and pay it back with a percentage of your business’s daily sales or with fixed daily withdrawals from your business’s bank account.

Instead of getting an interest rate, you’ll get a factor rate, which determines how much you’re on the hook to pay back upfront. Multiply your merchant cash advance by the factor rate and that’s how much you’ll pay.

Short term business loans could help your business in a pinch. Their fast turnaround time and relatively effortless applications mean you can get a small amount of funds fast when you need it. Your business will pay for that quick and easy application because they cost more than your typical business loan, so you might want to treat them as a last resort.

Curious about how other types of business financing work? Check out our business loans guide, where we break things down and compare lenders.

We explore the range of business loans available through Portman Finance.

Discover more about the business loans on offer from Love Finance.

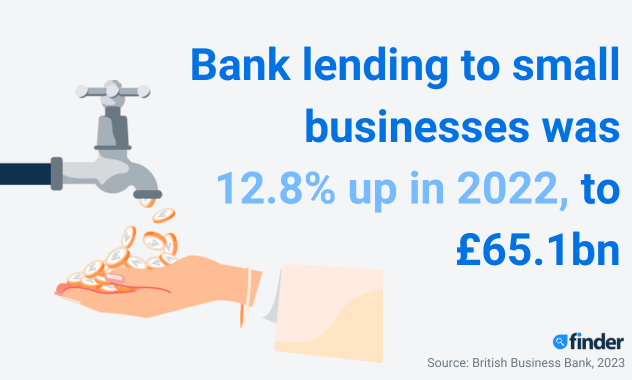

We look at the most recent business loan statistics and trends, and how lending to SMEs and small businesses has changed over the years.

Lombard helps businesses finance the equipment they need to grow, funding a wide range of assets from business vehicles to machinery.

Funding Options finds competitive credit for small businesses by searching its panel of over 50 trusted providers. Find out how other lenders compare.

Cubefunder offers business loans of up to £100,000 with one fixed fee. Repayments can adapt to the rises and falls of your company’s cashflow. Find out how other lenders compare.

Find out about the many business loans available from NatWest Bank.

Information about the business loans available from Barclays Bank.

Information about the business loans available from HSBC.

An overview of the range of business loans available from Santander Bank