See your personalised rates

Find lenders that can approve you

Good or bad credit histories considered

Fast funding with no hidden costs

Loans enable you to borrow a lump sum of cash that you then repay in fixed monthly instalments over a set term. They can be a popular way to borrow money to help you pay for a new car, consolidate existing debt or pay for home improvements.

If you apply for a loan, you’ll pay interest on your repayments. The amount of interest charged on your loan depends on a range of factors, including your credit score. The better your credit score and history, the more likely you are to qualify for the best rates.

By the same token, if you’re young and have yet to build up a credit history, you’ll likely struggle to secure the most competitive interest rates or even get accepted for a loan at all.

| Lender | Minimum age | Minimum income | Customer type | Link |

|---|---|---|---|---|

|

Lendable

|

18 | 9600 | New or existing customers | Check eligibility |

|

Guarantor My Loan

|

18 | 0 | New or existing customers | Check eligibility |

|

Evlo

|

18 | 10000 | New or existing customers | Check eligibility |

|

118 118 Money

|

18 | 8400 | New or existing customers | Check eligibility |

|

NatWest

|

18 | 0 | Existing customers only | Read our review |

|

Royal Bank of Scotland

|

18 | 0 | Existing customers only | Read our review |

|

Bamboo

|

18 | 0 | New or existing customers | Check eligibility |

|

HSBC

|

18 | 10000 | New or existing customers | Check eligibility |

|

Zopa

|

20 | 12000 | New or existing customers | Check eligibility |

|

Fluro

|

21 | 10200 | New or existing customers | Check eligibility |

|

My Community Bank

|

21 | 18000 | New or existing customers | Read our review |

|

AA

|

18 | 0 | New or existing customers | Check eligibility |

|

Shawbrook Bank

|

21 | 15000 | New or existing customers | Check eligibility |

|

Bank of Scotland

|

18 | 0 | Existing customers only | Read our review |

|

M&S Bank

|

18 | 10000 | New or existing customers | Check eligibility |

|

Barclays Bank

|

18 | 0 | Existing customers only | |

|

Ulster Bank

|

18 | 0 | Existing customers only | Read our review |

|

AIB (NI)

|

18 | 0 | Existing customers only | Read our review |

|

Halifax

|

18 | 0 | New or existing customers | Read our review |

|

Virgin Money

|

18 | No minimum income specified | Existing customers only | Read our review |

|

Nationwide BS

|

18 | 8400 | Existing customers only | Read our review |

|

Monzo Bank

|

18 | No minimum income specified | Existing customers only | Read our review |

|

Tesco Bank

|

18 | 0 | New or existing customers | Read our review |

|

TSB

|

18 | 10200 | New or existing customers | Read our review |

|

MBNA Limited

|

18 | 0 | New or existing customers | Read our review |

|

Abound

|

18 | 0 | New or existing customers | Check eligibility |

|

Lloyds Bank

|

18 | 0 | Existing customers only | Read our review |

|

First Direct

|

18 | 10000 | Existing customers only | Read our review |

|

Admiral

|

18 | 19000 | New or existing customers | Check eligibility |

|

Novuna Personal Finance

|

21 | 10000 | New or existing customers | Check eligibility |

|

Santander

|

21 | 10500 | New or existing customers | Check eligibility |

|

Creation Financial Services

|

23 | 9600 | Existing customers only | Read our review |

|

Minty Loans

|

21 years | No minimum income specified | Not specified | Check eligibility |

|

Fluent Money

|

18 | No minimum income specified | Not specified | Check eligibility |

|

Reevo Money

|

21 years or older | 15000 | Not specified | Check eligibility |

|

Plata

|

18 | 0 | New or existing customers | Check eligibility |

|

Finio Loans

|

18 | 0 | New or existing customers | Check eligibility |

|

Oakbrook Loans

|

18 | 0 | New or existing customers | Check eligibility |

|

John Lewis Money

|

20 | 12000 | New or existing customers | Check eligibility |

|

Munzee

|

21 | 0 | New or existing customers | Check eligibility |

|

Loans by Mal

|

21 | 15600 | New or existing customers | Check eligibility |

|

Norwich Trust

|

21 | 15600 | New or existing customers | Check eligibility |

|

Plend

|

21 | No minimum income specified | Not specified | Read our review |

|

Churchill

|

18 years | 10200 | Not specified | Read our review |

|

Toot Loans

|

23 years or older | 12000 | Not specified | Read our review |

|

BetterBorrow

|

18 years | No minimum income specified | Not specified | Read our review |

|

JustUs

|

18 | 12000 | New or existing customers | |

|

Danske Bank

|

18 | 0 | Existing customers only | Read our review |

|

LiveLend

|

18 | £12,000 per year | Not specified | |

|

Loans 2 Go

|

21 | No minimum income specified | Not specified | Read our review |

Turning 18 can be exciting. After all, you’ll now be legally allowed to vote and drink. You’ll also be able to take out a loan.

However, getting a first time loan as a young person may be more difficult than simply applying and getting approved. That’s because you’ll have little to no credit history which means lenders cannot assess how reliable you are as a borrower. You may also not have much in the way of savings. This means your loan options may be more limited.

But the good news is you may be able to access one of the following options:

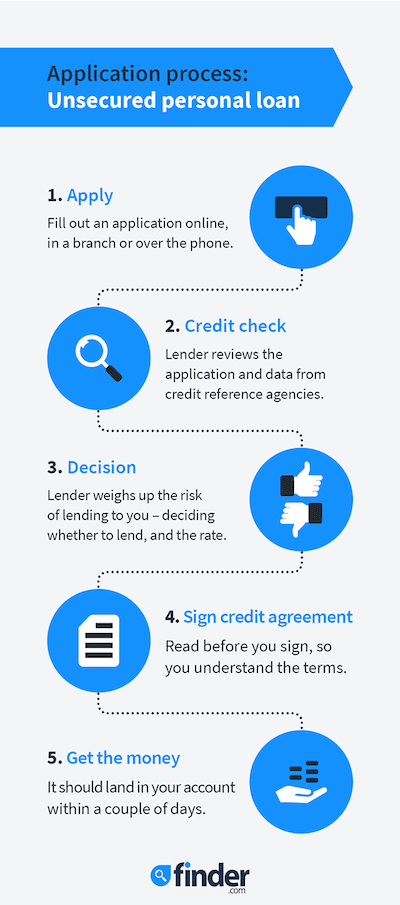

A personal loan lets you borrow a fixed sum of money over a set term and you repay this in monthly instalments. To increase your chances of getting accepted when you’re young, it can be worth applying for a loan with your current bank.

Because you’ll have already established a relationship with your current bank – perhaps you hold a bank account and a savings account with that provider – they might be more willing to give you a loan. The downside is that it might not offer the best rate on the market.

Alternatively, you could compare other lenders and use an eligibility checker or “soft search” which will show you the loans you’re more likely to get accepted for without damaging your credit score.

With a guarantor loan, a friend or family member guarantees the loan you apply for. This means that if you are unable to repay the loan, your guarantor will be responsible for paying it off.

If you’re looking to buy a car, there’s a number of different car finance options to suit a wide range of monthly budgets.

If you’re planning to go to university, you’ll be able to apply for student finance, including a tuition fee loan and a maintenance loan to help with your living costs. You’ll repay this loan once you’ve graduated and start earning above a certain income threshold.

If you’re a student, there are student bank accounts available with favourable overdraft terms. If you’re not, an arranged overdraft can offer you flexibility but you’ll want to look closely at the fees and interest charges involved.

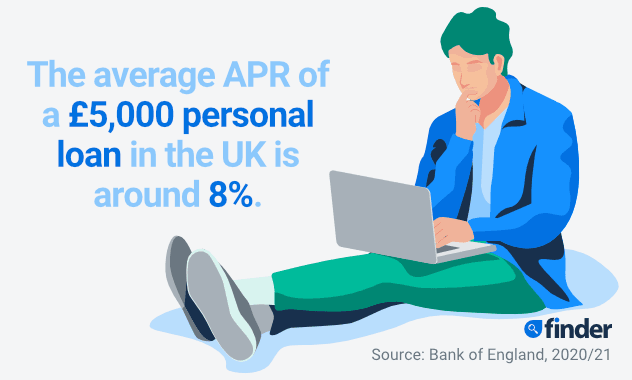

Loans for young people work in the same way as any standard loan. You borrow a sum of cash (usually between £1,000 and £25,000) and you then pay back that amount in monthly instalments, with interest added on top. Personal loan terms typically range from 1 to 7 years.

If you’re a young person with a limited credit history, the amount of interest you pay on your loan will likely be higher compared to someone who has an established credit history. Most personal loan rates are fixed, so your monthly repayments remain the same during the term of the loan.

Be aware that if you want to pay off your loan early, you’ll often be charged a penalty fee (sometimes referred to as an early repayment charge).

Before taking out a loan it’s crucial to work out whether you would be able to afford to repay it. This can be much harder when you’re young because your financial circumstances are likely to be more changeable and less established.

Taking out a loan comes with risks, and it’s important to understand these risks before you dive in. Get it wrong, and you could land yourself in serious financial difficulty or damage your credit record – making things much harder when you need to get a loan in the future.

Consider whether you really need to borrow the money and if you do, whether you could use an alternative, cheaper option such as a credit card or overdraft. If you still want to apply for a loan, it’s a good idea to start small and borrow a small amount over a short term.

Yes, once you turn 18, you’re eligible to take out a loan or other credit product. Whether you’ll be able to get a loan will depend on a range of factors, such as:

Your credit score is used by lenders to determine your creditworthiness. If you have a good credit score, this indicates to lenders that you have paid back debts in the past and have not missed payments. The higher your credit score, the more likely you are to get accepted for a loan.

It can be harder for young people to take out loans simply because you’re likely to have a limited credit history. This means lenders will have difficulty assessing your creditworthiness and how responsible you are as a borrower. Without knowing how likely you are to repay the loan, lenders will be more reluctant to offer you money.

Because lenders will view you as higher risk, if you are accepted for a loan, you’ll probably pay a higher interest rate and you might not be able to borrow as much.

If you get accepted for a loan and repay it on time, your credit score will gradually improve. However, if you miss payments and default on the loan, this will be recorded on your credit report which could negatively affect your credit score.

Your employment status could be another reason why it’s harder to be accepted for a loan. Lenders tend to favour borrowers who have remained in the same job for a few years as this stability reassures them that you’re more likely to meet your monthly loan repayments.

Firstly, check you’re registered on the electoral roll as this will show lenders you have a fixed address. Next, check your credit report to see if there are any errors. If there are, contact the credit reference agency to get them corrected.

Also ensure you pay bills on time and if your landlord includes your bills in your rent, ask if your name can be put down on some of them.

At Finder, we run soft searches with a range of lenders in seconds, meaning that you’ll be able to get realistic rate quotes for loans you’re likely to be approved for, without any impact on your credit score. This can be a really smart way to avoid disappointment, protect your credit record and to only focus on lenders who are likely to approve you.

The quickest and easiest way is to use Finder’s personal loan comparison tables. Compare interest rates carefully and aim to keep the overall cost as low as possible, while ensuring you can still afford the repayments.

Once you’ve found a suitable loan, use an eligibility checker to check your chances of being accepted for the loan, whether there are any fees and how much you will be able to borrow.

A broker will find the best rate available to you from its panel of lenders, taking into account your individual circumstances. Normally this service is free, because the broker will earn a referral fee from the lender.

As long as you bear in mind that they don’t normally scan the whole market and will use selected lenders, a broker can take the strain out of finding a competitive deal.

Used correctly, credit builder cards can help you to improve your credit score over time. However, they typically come with low credit limits and high interest rates so it’s important to pay off your balance in full each month.

Alternatively, you could speak to your bank about extending your overdraft and asking for more favourable conditions. Interest rates on overdrafts can be high so they may not always be the best option.

Taking out a loan can be an easy way to borrow extra funds and, providing you’re sensible, it can also help to build up your credit score. However, interest rates can be high and if you’re unable to keep up with your repayments, you could do your credit score more harm than good. Always consider your options carefully before applying.

Discover the most reliable means for migrants and international students to borrow money in the UK

Our guide explores all the best options for getting a loan when you’re an apprentice.

If you have just started a new job, you could still be accepted for a personal loan. See how lenders compare and give yourself the best possible chance of being accepted.