Check your eligibility with lenders

Good or bad credit histories considered

Fast funding with no hidden costs

One simple form to compare lenders

We currently don't have that product, but here are others to consider:

How we picked theseTo make it even easier to compare and evaluate unsecured loans we came up with the Finder Score. Speed, features and flexibility across 60+ lenders are all weighted and scaled to produce a score out of 10. The higher the score the better the lender – simple.

Read the full methodologyPlease note: You should always refer to your loan agreement for exact repayment amounts as they may vary from our results.

Late repayments can cause you serious money problems. See our debt help guides.

Getting a £3,000 loan will depend on your status, whether you have a good, fair or poor credit score but there are different providers that cater to each. This guide compares the best loans on the market, tools to see if you’re likely to get approved for the loan (our LoanFinder tool) and a calculator to check how much you’ll eventually repay.

Whether you’re planning a holiday abroad or perhaps need to repair your car, a £3,000 loan can let you spread the cost over a time frame that suits you. It’s a figure that can be small enough to pay back without making major lifestyle changes. Many lenders reserve their best rates for larger loans, however, so it is worth taking the time to find the best deals available to you. Here’s how.

Loans of this sum are available from a huge range of lenders, both traditional (high street banks) and non-traditional (online specialist lender offering loans for bad credit). The providers and products you can choose from will be determined by factors such as your circumstances and the purpose of the loan. Perhaps the most common option, however, is an unsecured fixed-rate personal loan.

With an unsecured loan, the borrower doesn’t put down any possession as collateral. By contrast, a loan that involves collateral is called a secured loan. The most common examples of secured loans are for larger amounts, such as mortgages (where a property is used as collateral) and car finance (where a vehicle is used as collateral). However, it’s worth noting that even when a loan is unsecured, the lender can take legal action to get its money back.

Unsecured loans involve less risk for the borrower, but more for the lender. As such, they can involve higher rates than secured loans.

A fixed interest rate will not change throughout the course of a loan. It’s the opposite of a variable rate, which can be changed at the lender’s discretion. A fixed interest rate means equal monthly repayments. Each repayment consists partly of the interest accrued so far, and partly of a repayment towards the original sum borrowed.

Each lender will offer a range of loan terms, and normally the term that you opt for will be dictated by the affordability of monthly repayments. Broadly speaking, the shorter the loan term, the higher your monthly repayments will be. If you opt to spread the repayment over a longer loan term, your monthly repayments will be more manageable, but the overall cost of the loan will be higher.

There are occasional exceptions to this rule, however – such as when a lender offers a promotional, lower rate on specific loan terms or loan amounts. Sometimes, by increasing the loan term or loan amount fractionally, borrowers can access a better rate. By focusing on the “total amount payable” (that’s the overall cost of the loan) it’s straightforward to work out your smartest course of action.

Here’s an example of a £3,000 loan over two years at a 9% APR. Each bar represents a single monthly repayment, and you can see how the breakdown of interest vs. capital changes over the course of the loan.

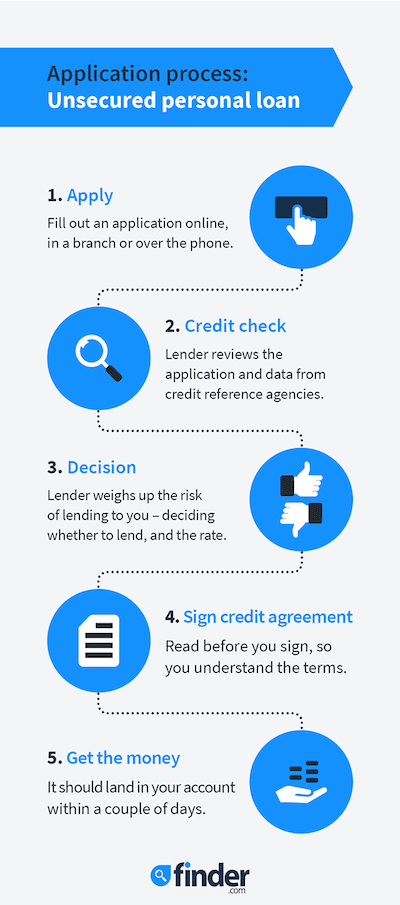

These are some of the key steps on your journey to securing a £3,000 loan:

If you have a bad credit rating, there are still lenders out there who will help you. Typically, specialist loans for people with bad credit will have extra high rates and/or require a guarantor.

It used to be tougher for self-employed people to get a personal loan, because in many cases, their income was deemed too unreliable. However, the demand for loans among self-employed people has grown so much that there are now lenders who specialise in offering deals to them.

It’s often stated in personal loan terms that the money can’t be used to fund a business. However, there are a range of specialist business loans and lenders around, too, many with features specifically tailored to business purposes.

Here are the key factors to consider when comparing personal loans.

It is possible to apply for a credit card with a £3,000 limit. There are even some cards that’ll offer you an introductory period where you pay 0% interest on purchases, although, once again, approval will depend on your credit rating. Nevertheless, if you feel confident about being approved for these cards, you could potentially receive a £3,000 “loan” without paying any interest. Ensure you pay off your debt before the introductory 0% period comes to an end, though, because the rate will skyrocket at this point. If you can’t get hold of a 0%-on-purchases credit card, compare the available rates with those offered by personal loan companies. In many cases, you’ll pay more on plastic.

| Interest rate of 5.0% fixed p.a. | Interest rate of 10.0% fixed p.a. | Interest rate of 25.0% fixed p.a. | |

|---|---|---|---|

| 1 year term | £256.82 monthly £3,081.87 overall | £263.75 monthly £3,164.97 overall | £285.13 monthly, £3,421.59 overall |

| 2 year term | £131.61 monthly £3,158.74 overall | £138.43 monthly £3,322.43 overall | £160.11 monthly, £3,842.75 overall |

| 3 year term | £89.91 monthly £3,236.86 overall | £96.80 monthly £3,484.86 overall | £119.28 monthly, £4,294.06 overall |

As well as your credit record, lenders will consider:

If you need to borrow £3,000, it’s wise to compare your options first. You’ll want to look at the interest rates, term lengths, the total amount payable, any fees or penalties, and the restrictions, if any, around making early repayments.

Before applying, make sure you meet the lender’s criteria to give you the best chances of getting approved.

Most students have to operate on a shoestring budget, but when a financial shortfall hits, thankfully there are a number of options to consider.

Looking for online peer-to-peer lending platforms? Here’s a list of similar companies to Zopa with example loans and lender terms.

Looking to borrow money without using a guarantor? It’s possible, even if you have a bad credit score

With ever-rising public transport costs, it’s more important than ever to find the cheapest way to fund your commute. Here’s how to weigh up the options and find what works for you.

Want to be able to game whenever you go, but not sure you can afford to splash the cash on a gaming laptop? From in-store finance to personal loans, check out our guide to finding the right loan for you.

Taking out a joint personal loan is a major commitment, but one that could help you to borrow larger sums at competitive rates.

RateSetter might be the biggest name in peer-to-peer lending right now, but it isn’t alone in this growing sector. Compare similar platforms offering competitive rates to borrowers and investors alike.

Looking for a personal loan? Read the definitive guide to find out how to compare interest rates, fees and features to find the right loan for you. There’s a range of loans available to apply for – we’ll help you find the right one.

Whether you have good or bad credit you could get approved for a £10,000 personal loan. Compare the best lenders for your individual circumstances.

Compare Post Office fixed-rate personal loans against products from a range of UK lenders. Apply online and secure a competitive rate.