Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

When you choose to remortgage your existing mortgage, you should take into account the amount of equity you’ve built up in your home. If you don’t have enough equity, remortgaging could be a bad idea.

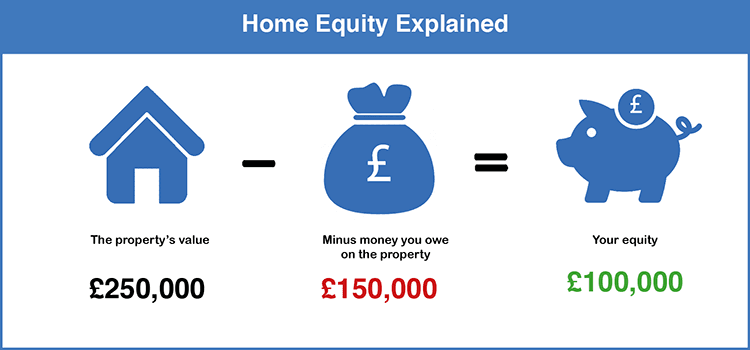

What is equity?

When you make payments towards the principal amount of your mortgage you build up equity in your home. The equity is the difference between your home’s value and what you have left to repay on your mortgage. This is the money you can expect to keep if you sell your home and repay your mortgage with the proceeds from the sale.

How much equity do I need when remortgaging?

Many loans come with a maximum loan-to-value (LTV) ratio of 95%, which means you cannot borrow more than 95% of the value of your home. What this also means is that if you wish to remortgage you must have at least 5% equity in your home.

To put yourself in the best position to remortgage, you should have at least 20% equity in your home.

Applying for remortgaging with no equity is difficult unless you can get someone to be a guarantor.

Remember that lenders look at your equity as a means to assess risk. The more equity you have, the less of a risk you are to the lender and vice versa.

What if I don’t have at least 20% in equity?

When you choose to remortgage without at least 20% equity in your home, the lender is less likely to approve your application to remortgage. If you are approved, you will likely be charged a higher interest rate than you would be if you had 20% equity. This is because the more equity you have, the less of a risk you are to the lender.

Alternative options

Before comparing remortgaging options, find out how much equity you have in your home. If you don’t have a 20% deposit saved but aren’t far off the mark, it might make sense to wait until you’ve built up a higher amount of equity.

Alternatively, you can consider applying for a guarantor mortgage or applying with specialist banks that may have less stringent lending criteria for remortgage mortgages.

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Matthew Boyle is a banking and mortgages publisher at Finder. He has a 7-year history of publishing helpful guides to assist consumers in making better decisions. In his spare time, you will find him walking in the Norfolk countryside admiring the local wildlife.

See full bio

Matthew's expertise

Matthew

has written

224

Finder guides across topics including:

Helping first-time buyers apply for a mortgage

Comparing bank accounts and highlighting useful features

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.