Please note: You should always refer to your loan agreement for exact repayment amounts as they may vary from our results.

Late repayments can cause you serious money problems. See our debt help guides.

We currently don't have that product, but here are others to consider:

How we picked theseTo make it even easier to compare and evaluate unsecured loans we came up with the Finder Score. Speed, features and flexibility across 60+ lenders are all weighted and scaled to produce a score out of 10. The higher the score the better the lender – simple.

Read the full methodologyPlease note: You should always refer to your loan agreement for exact repayment amounts as they may vary from our results.

Late repayments can cause you serious money problems. See our debt help guides.

While the term “student loans” is generally used to mean the government-supported finance offered to students in the UK, it can also refer to any private personal loans or other forms of credit that students are eligible for.

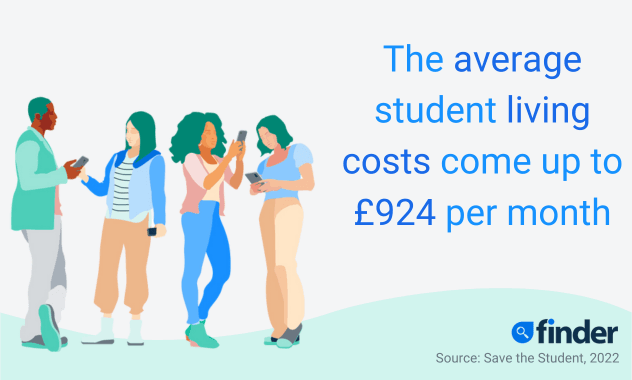

If you’re a student, chances are you’re used to operating on a shoestring budget even if you have a part-time job. This means your bank account balance may end up looking a bit grim if any unexpected costs come up during your studies. When you find yourself short of funds, one option is to borrow money from friends or family to avoid having to pay interest. But if the Bank of Mum and Dad is closed and you still need money, you might want to consider the following alternatives.

Private student loans are those taken out with a lender or loan provider, and not offered through the government. They are generally unsecured personal loans, which let you borrow an agreed amount and then repay it over a fixed term, usually 1-7 years. Private student loans can be used to cover the cost of tuition and student fees, as well as any other expenses you may have, such as accommodation, food and other living costs.

While most credit cards will be off limits to the majority of students due to their limited credit history and low income, these targeted cards are easier to get approved for. Expect a wide range of interest rates across the cards on the market, with some offering 0% interest on purchases for a set period before ramping up the rate later on.

The best strategy with student credit cards is to use them and pay off your balance as soon as possible afterwards – do this every month and you shouldn’t be charged interest, even if it’s not a 0% card. Don’t use it to withdraw cash, as then you’ll start paying interest immediately and incur fees.

Designed as a “stepping stone” product for borrowers with a poor or limited credit history, these credit cards don’t come with a 0% introductory period, and generally have a high interest rate. However, as the name suggests, these cards can help build your credit rating, which may make you more likely to be approved for another credit card or personal loan in future.

Taking out a traditional personal loan as a student requires careful consideration. Some lenders will not consider applications from students, and those that do will likely want you to have a strong credit rating. Lenders want to be sure that you’re likely to be able to repay your loan, and this may be hard to prove if you have no real credit history or a stable source of income.

More importantly, if you are approved for a personal loan, you’ll need to make sure that you can definitely afford your loan repayments.

With a guarantor loan, a friend or relative promises to step in if you fail to keep up with your repayments. These loans are offered by specialist lenders, and typically come with a high rate of interest. Again, you’ll need to be able to demonstrate that you’ll be able to afford your repayments.

Payday loans and short-term, high-cost instalment loans can be relatively easy to be approved for, but have an eye-wateringly high rate attached – up to 0.8% per day. As such, they should only be considered as a last resort. Some lenders, such as Smart-Pig, target students specifically, focusing on your next student loan instalment, rather than your next payday.

This will depend on your individual circumstances and the type of loan you have. Government student loans have standardised interest rates, but these vary based on when you studied, and can also be changed retroactively. Personal loans offer different rates depending on the lender, as well as things like the size and term of your loan, and your credit history. You can compare student personal loans here.

Like with any loan, the best student loan will be the one that offers the most competitive interest rate and repayment terms. While government student loans may offer favourable repayment terms, these loans are not available to everyone. You may find you’re able to secure a student loan with a lower rate elsewhere.

You can read our list of the best tips to keep in mind when comparing student loans below.

All lenders will put applicants through both a search with a credit reference agency (CRA) and their own internal affordability and risk assessments. As a student, you may have a very limited credit history – especially if you’ve gone straight from school into higher education, and/or a lower income.

Your circumstances may also be considered more changeable (and therefore more risky) to a lender, and realistically it can be harder for you to get access to traditional credit. The good news, however, is that many of the options above are specifically tailored to people in your situation.

Always check the eligibility criteria of the specific product you are considering before applying – as well as wasting your time, multiple applications for credit in a short space of time can damage your credit score. Most lenders now offer a “soft search” facility, where would-be borrowers can check their likelihood of being approved for a loan or credit card before submitting a full application, and without affecting their credit record.

While there is no guarantee that you’ll be rejected, it may be difficult to get approved for a personal loan if you’re a student with bad credit, especially if you aren’t earning an income. If you’re young and have a bad credit score, the lender may consider you to be too high a risk when it comes to repaying your loan. If you want to check if you’ll be able to get a loan with bad credit, you can find out your loan options here.

If you find that you won’t be able to get a personal loan with your credit rating, you may want to apply for a payday loan. Short-term lenders do not place the same importance on credit score, and are therefore more likely to approve you for a loan.

However, payday loans should only be considered as a last resort, and failing to repay a short-term loan can cause financial stress. It will generally be a better idea to try and improve your credit score and then apply for a regular personal loan.

You may not have realised that you can improve your credit record by getting on the local electoral roll, and by setting up a current account with a few direct debits. If you can put a little into savings each month, even better, although that’s simply not possible for many students.

Perhaps the most important thing you can do is to keep up with any bill payments and not dip into an unauthorised overdraft. Such actions will remain on your credit record for a number of years.

Always try all the 0% interest options first when you’re looking to borrow money. These could be loans from friends and family, a hardship fund, an arranged student overdraft or a student credit card. With the latter two options, the interest will eventually ramp up, so it’s best to pay it back before that point.

Only when all of these options are exhausted is it time to consider high-interest options such as credit-builder credit cards or personal loans. In this situation, it’s useful to compare the amount of interest you’ll owe, while also considering what form of credit you’re likely to be considered for.

With all these options available, a short-term financial shortfall shouldn’t be the end of the world for you. By searching for the best loan option and paying your debt on time, you’ll hopefully be back on your feet in no time.

Discover whether you’re eligible for student finance, how much money you might get and how the repayments work with our ultimate guide to student finance.

Discover the most reliable means for migrants and international students to borrow money in the UK

If you’re planning to apply for a personal loan, credit card or mortgage, find out how student loan debt could affect your ability to be approved.

Looking for online peer-to-peer lending platforms? Here’s a list of similar companies to Zopa with example loans and lender terms.

Looking to borrow money without using a guarantor? It’s possible, even if you have a bad credit score

With ever-rising public transport costs, it’s more important than ever to find the cheapest way to fund your commute. Here’s how to weigh up the options and find what works for you.

Want to be able to game whenever you go, but not sure you can afford to splash the cash on a gaming laptop? From in-store finance to personal loans, check out our guide to finding the right loan for you.

Taking out a joint personal loan is a major commitment, but one that could help you to borrow larger sums at competitive rates.

RateSetter might be the biggest name in peer-to-peer lending right now, but it isn’t alone in this growing sector. Compare similar platforms offering competitive rates to borrowers and investors alike.

Looking for a personal loan? Read the definitive guide to find out how to compare interest rates, fees and features to find the right loan for you. There’s a range of loans available to apply for – we’ll help you find the right one.

Whether you have good or bad credit you could get approved for a £10,000 personal loan. Compare the best lenders for your individual circumstances.

Compare Post Office fixed-rate personal loans against products from a range of UK lenders. Apply online and secure a competitive rate.