Good home insurance can give you confidence that you’re financially protected if your home or its contents are damaged or destroyed, or if you’re the victim of theft or burglary. But the level of cover can vary, so it’s important to do your research before you buy.

What is home insurance?

Home insurance is designed to cover any unexpected harm to your home and belongings. It means that if your house or flat – or its contents – are damaged or destroyed, or if valuable items are stolen during a burglary, you will receive a financial payout to cover the cost of all or some of your loss. This will enable you to repair or rebuild your home or to replace your belongings.

Home insurance jargon explained

Certificate of home insurance. A document you get from your insurer that provides legal evidence that you’re insured. Duty of disclosure. A requirement for you to tell the insurer about anything that might affect your policy. This applies both when you take out the policy and if anything changes, such as an increase in the number of people living in your home. Sum insured. The maximum amount that will be paid out towards repairing or rebuilding your home, or replacing your belongings. The sum insured amount is set when you take out your policy. Proof of ownership. A document, such as a receipt or a photo of you with an item, that proves that you owned something you make a home insurance claim for. This is particularly important for high-value items.

How to compare home insurance

To compare home insurance policies effectively, you’ll need to follow a few simple steps.

Think about your basic cover needs. Before you start shopping for a policy, consider the risks you want to cover and the level of protection you need. For example, do you need both buildings and contents insurance? What is the value of your home and belongings, including individual valuable items, and how does this affect the level of cover you need? Once you’re clear on the type of home insurance you’re after, you can start looking for the right policy.

Decide which optional extras you want. Some policies include various “add-ons” as standard, but more often you’ll need to pay extra. If you like the sound of accidental damage or personal possessions cover, for example, make sure you take account of any additional costs when you compare home insurance policies.

Use a price comparison site such as Finder to compare policies. Don’t automatically settle for the first, or cheapest, policy you find. Instead you should compare the benefits, costs, features and exclusions of a wide range of policies to work out which option provides the best value for money. Bear in mind some insurers aren’t on price comparison sites, so you may need to check a handful directly to get a complete picture. If you have an unusual or high-risk property – for example a house with a thatched roof, or with a history of flooding – you may benefit from using a specialist insurance broker.

Ask for recommendations. Check out online reviews, and ask friends and family for their home insurance recommendations. Home insurance only proves its worth when you need to make a claim. So, hearing from people who have actually had to make a claim on their policy is a great way to sort the strong policies and insurers from the weaker ones.

Read the policy docs. Don’t wait until it’s time to make a claim to check your policy documents. Read the terms and conditions of shortlisted insurers (or at very least the summary) before you buy the policy. This will allow you to determine exactly what the policy includes, how much protection it offers, and under what circumstances cover would not be provided.

How can I save money on my home insurance?

It is important to remember that the cheapest home insurance isn’t necessarily the best home insurance. An ultra-cheap policy could prove a false economy if it doesn’t pay out when you need to claim. If you’re looking for the best value insurance cover for your home, the single most important thing you can do is compare home insurance policies. Shop around for the best deal on the right kind of policy for you. This will help you make sure you are getting true value for money.

Practical ways to keep costs down include:

Review cover and compare policies regularly. Just because a particular insurance policy was right for you a few years ago doesn’t necessarily mean it’s the right fit for you now. Cover needs change all the time. Maybe you’ve just invested in a top-of-the-line home entertainment system and want to upgrade your contents cover. In addition, insurers are constantly updating policies and premiums. Don’t be afraid to compare your options every year and see if you can find a better deal.

Choose a higher excess. If you are given the option, you might want to consider opting for a higher excess in return for lower premiums. Bear in mind that, if you need to make a claim, you may regret setting your voluntary excess extremely high in order to reduce your premiums by a relatively small amount.

Don’t add options you don’t need. Adding optional extras to your policy allows you to tailor home insurance protection to your requirements. Unfortunately, it also increases the premium, so make sure anything you add is absolutely essential.

Build up a no-claims bonus. Most insurers will give you a discount on your premiums for every year you don’t make a claim. Sometimes making a claim is unavoidable, but you can minimise the risk by taking care with your home and belongings, and keeping up with maintenance. You may also decide not to submit a claim for minor damage that you can afford to repair yourself.

Take advantage of discounts. Home insurers offer a variety of discounts to customers. These include discounts for having multiple policies with the insurer or for purchasing online.

Improve your home’s security. Simple things like installing a burglar alarm or extra door locks could help reduce your premiums. It reduces your risk for the insurer and you are likely to rewarded with lower premiums.

Pay annually. Insurers tend to charge more if you pay your premiums monthly rather than in a single annual sum.

What types of home insurance are there?

There are 2 main types of home insurance. If you own the property you live in, you’ll need to have both types to be fully protected.

You can buy buildings insurance and contents insurance as separate policies, or together as a combined home insurance policy. The best choice depends on your personal circumstances. Combined policies are more convenient and often cheaper, but may not be practical if you live in a flat where the buildings insurance policy is shared between multiple flat owners, for example.

Home insurance can feel like a necessary evil, and it can be tempting to cut corners and opt for lower levels of cover to keep premiums down.

But try to resist the temptation to underinsure just to save a few pounds. Buying insurance with too-low limits could come back to bite you if, for example, you need to make a claim and find that your £10,000 worth of belongings are only covered to a maximum of £5,000.”

What does home insurance cover?

The situations covered by your home insurance will vary depending on the insurer you choose and the level of cover you opt for, so you’ll need to compare home insurance policies carefully. However, the best policies generally provide cover against the following as standard:

Theft or burglary. If criminals target your home, you’ll be covered for loss or damage caused by theft, attempted theft or burglary.

Malicious acts and vandalism. If your home or contents are damaged due to vandalism or a malicious act, your policy will cover you.

Riots or civil commotion. Loss or damage caused by a riot, civil commotion, or industrial or political disturbance.

Burst pipes and other water damage. When water or oil escapes from gutters, pipes, baths, toilets, appliances or a range of other household items, home insurance covers you for the resulting loss or damage to the property itself (buildings insurance) and your belongings (contents insurance).

Flood. Loss or damage caused by water that has escaped the normal confines of a lake, river or a number of other bodies of water. Some home insurance policies only offer flood cover as an option, not as an automatic inclusion, so make sure you check your policy documents.

Fire. If your home and/or contents are lost or damaged due to fire.

Storm. Loss or damage caused by a storm, including violent winds, hail, snow, rain, or thunderstorms.

Lightning. Loss or damage caused by lightning, or by a power surge caused by lightning.

Earthquakes. This benefit ensures that you are covered against loss or damage caused by an earthquake.

Explosion. Loss or damage caused by an explosion, or a landslide or subsidence that occurs as an immediate result of an explosion.

Impact damage. This benefit covers you against impact from objects such as falling trees, power poles, TV antennas, motor vehicles and meteorites.

Subsidence. This offers support if the foundations of your property give way, gradually or over time, causing cracks in the walls or other damage.

What are home insurance optional extras?

Home insurance add-ons are extra elements of cover that aren’t typically part of standard home insurance cover. Depending on the specific policy, some insurers may include some of these elements in your premium. But, more commonly, you’ll need to pay an additional premium for each add-on.

Common add-ons include:

Accidental damage. It may seem surprising, but not all accidental damage is covered as standard by a home insurance policy. Many policies cover accidental damage to specific items – fixed glass, ceramics and mirrors, and home entertainment equipment are typically covered, for example. But many other mishaps, caused by members of your household, pets or visiting friends, aren’t usually covered as standard. So if you want to be protected against a dinner guest spilling red wine over a cream sofa or a DIY disaster, you’ll need an accidental damage add-on. You can take out accidental damage cover for both buildings and contents.

Bicycle cover. Bikes up to a certain value might be covered as standard in your home insurance policy, but there’s likely to be a limit on how much an insurer will pay out, and bikes may not be covered when you’re out and about. A bicycle add-on can offer reassurance that your wheels are fully protected, as long as you’ve left your bike securely locked up.

High-value items. Your standard home insurance policy will only cover valuables – such as jewellery or art – up to a certain limit. There will usually be a per-item limit, and an overall limit. If you own valuables that exceed either of these limits, you can pay extra to insure them as named items.

Home emergency. This covers the immediate cost of dealing with home emergency problems. These could include, for example, fixing a broken boiler or a burst pipe or, in some cases, sorting out a pest infestation. Bear in mind that home emergency cover won’t pay for the cost of damage to the structure of your home or your belongings as a result of the emergency, such as water damage to walls as a result of a burst pipe. That will be covered by your regular home insurance policy.

Legal expenses. This typically covers the cost of legal proceedings relating to your property, such as a dispute with a tradesperson over shoddy work or a boundary dispute with a neighbour. It often also covers legal expenses incurred as a result of employment disputes or if someone is injured in your property.

Personal possessions. Standard contents insurance only covers you for belongings inside your property. The personal possessions add-on extends cover to portable items you take out of your home, such as jewellery, your mobile phone, laptop and other gadgets.

Protected no-claims discount. As is also the case with car insurance, for every year you go without making a claim on your home insurance, you build up a discount on following years’ premiums. If you haven’t made a claim for a few years, this discount could be worth a fair amount. The no-claims discount protection add-on means that you won’t lose your discount if you make up to a certain number of claims.

Is home insurance worth it?

Home insurance isn’t a legal requirement, but if you don’t have it, you risk losing everything if the worst happens – if your home burns down in a fire, for example. Even if the loss is less extreme, the cost of home insurance is a small price to pay for the peace of mind that you’re financially covered for any damage to your property or its contents.

If you have a mortgage, it’s likely to be a condition of the loan that you must have buildings insurance on the mortgaged property.

If you rent your home, you don’t need to pay for buildings insurance as that’s the landlord’s responsibility. However, particularly if you are furnishing the property yourself, you may want to take out contents insurance to cover your belongings.

Pros and cons

Pros

Financial protection if your home or its contents are damaged or destroyed

Option to add cover for portable items outside of your home

Peace of mind that you won’t be left shelling out, potentially, hundreds of thousands of pounds.

Cons

There are some surprising exclusions from standard cover, such as many types of accidental damage

Excesses can mean that it may not be worth putting in a claim for lower-cost loss or repairs

You’ll often need to pay extra to cover high-value items.

Frequently asked questions

Purchasing your policy

Home insurance is something every homeowner should consider buying. It offers crucial financial protection for your home and important possessions. It can protect you against everything from fire and storm damage to burst pipes, falling trees, theft and vandalism.

If you’re not sure whether to take out home insurance, think for a moment about how you would cope financially if your home and everything you own was completely destroyed. The cost of rebuilding your home and replacing your belongings could run into hundreds of thousands of pounds.

Sure, it’s a worst-case scenario and one that you’ll hopefully never have to deal with, but would you have the financial means to start again from scratch following an unexpected disaster? Taking out buildings and contents insurance offers:

Protection for your home. Your home is usually the most expensive thing you’ll ever buy and, therefore, the most valuable asset you’ll ever own. Buildings insurance provides a level of protection for your home should certain unexpected disasters strike. It means that in the event of damages or loss, you’ll be able to claim to repair or restore your home. Plus, most mortgage lenders require you to have buildings insurance in place before they’ll lend to you.

Protection for your possessions. The possessions within your home are much more than just stuff. They’re often your most important and treasured belongings, and can hold just as much sentimental value as they do financial worth. Contents insurance ensures that you will be able to repair or replace your possessions if they’re damaged by fire, storm, theft or a range of other insured events. This type of insurance is usually available as standalone cover, or as part of a combined home and contents policy.

Peace of mind. The biggest benefit of home insurance is the reassurance it provides. With the right policy in place, you can relax knowing that you will have the financial support you need should loss, damage or some other unexpected misfortune affect your home or contents.

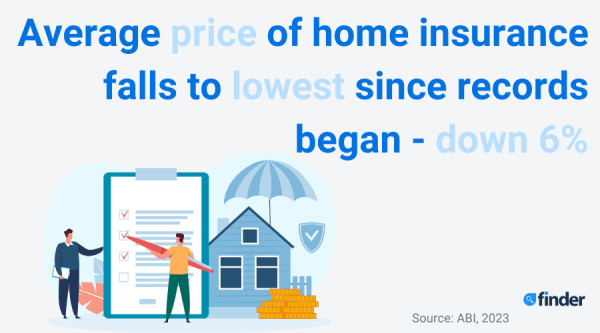

As of July 2023, the average cost of home insurance in the UK was around £212 a year for combined buildings and contents insurance, according to financial insight firm Consumer Intelligence. However, the cost of your policy may differ based on the type and level of cover you require, as well factors such as:

The sum insured. This is the maximum amount that your insurance company will pay in the event your home is totally destroyed. The higher the sum insured, the more your premium will be. For example, if you want to cover your home to the tune of £1 million, don’t be surprised if your premiums are much higher than they are for someone who selects a sum insured of £300,000.

The options you select. If you choose to tailor your policy to suit your needs by adding extra-cost options, your premiums will also be more expensive.

Amount of excess. Many insurers offer a flexible excess on home insurance policies, allowing you to choose a higher excess in return for lower premiums.

Your home. Insurers will consider the age and construction of your home when calculating your premiums. This will help them determine how likely it is to withstand damage and how much it will cost to repair or rebuild.

Where your home is located. If you live in an area prone to crime or floods, you may find that the increased risk of damage will push up your premiums.

Security features. Insurance underwriters consider how well your home is protected against theft and burglary. Installing a back-to-base security alarm is one way to reduce the cost of your premiums.

Your claims history. If you’ve previously made multiple claims on a home insurance policy, you can expect higher premiums when you take out a new policy.

A home insurance excess is the amount you contribute in the event of a claim. It’s usually broken down into 2 elements – a compulsory excess, which you can’t change, and a voluntary excess, which you can adjust during the quote process. The higher the voluntary excess, the lower your premiums will be, but the more you’ll have to pay in the event of a claim.

Some areas of cover may be subject to higher excesses than others. For example, subsidence and flood damage often have much higher excesses than other buildings insurance claims.

It is important to be aware of what isn’t covered under home insurance. Exclusions that are important to be aware of include:

“Existing damage” (any loss or damage that happened before cover started)

Damage that is the result of wear and tear or inadequate home maintenance.

Failure of computers or other electrical equipment due to viruses.

Deliberate acts – so any loss or damage intentionally caused by you or someone lawfully in your home.

Exclusions that will, hopefully, only apply in rare circumstances include damage caused by war, radioactive contamination, sonic bangs, pollution, and terrorism.

There are a number of factors that will help determine the right home insurance policy for you. This includes whether you’re an owner-occupier, renter or landlord, and whether you want to just protect the property itself, your possessions or both.

If you own your home, the type of building – as well as any additional features such as a garage or yard – may also affect the type of cover you may need. There are a few different types of home insurance and they each provide cover against different things.

Finding the best home insurance policy is a matter of understanding your situation and needs, as well as your budget and risk tolerance.

Home insurance policies typically last for a year. Most insurers will let you pay your premium on a monthly or yearly basis. While it may be tempting to choose a monthly premium, it will generally be cheaper to pay for the full year up front, as paying in monthly instalments will incur interest.

Contents insurance covers damage to or loss of the moveable belongings inside your home, such as furniture, electrical items and clothes. Buildings insurance covers damage to the structure of your home (the walls, floors and roof) and any fixed fittings (the units in your bathroom, for example).

Yes, you are free to insure multiple properties. It’s a good idea to get insurance policies for each of the houses you own or occupy (all or some of the time).

When you purchase a buildings and/or contents insurance policy, you are generally able to set the “sum insured”. This is the total amount you would be covered for in the event your house or possessions are destroyed or need to be repaired.

It’s important that your sum insured amount is high enough to cover the likely cost of rebuilding your home or replacing your items. Otherwise you will be required to make up the difference using your own savings. Specific types of claims, such as key and lock replacement, will also have individual cover limits.

Water leaks are the most common cause of insurance claims. Many policies do cover water leaks, otherwise known as “escape of water”, but it depends on the policy and what’s caused the leak (for example, leaks caused by poor maintenance may be excluded), so read the small print carefully.

It depends how long you’re away for. Most home insurance policies state that you must not leave your home unoccupied for more than 30 or, in some cases, 60 days. If you take lots of long trips, check the terms. Houses that are unoccupied for very long periods of time will not be covered under regular home insurance. If you’re insuring a second home that you only spend part of the year in, consider specialist holiday home insurance.

Probably. However, depending on the reason for the subsidence, you may find that fewer insurers are willing to cover you due to the higher risk your property poses. If you can get cover, subsidence may be excluded. If subsidence is covered, expect your premiums to be higher, particularly if there have been claims for subsidence on your property in the past. Excesses are also likely to be high. If you struggle to find affordable cover for a property with subsidence, a broker may be able to help. Try the British Insurance Brokers’ Association’s “Find a Broker” service.

Yes, but many insurers don’t offer standard cover for such properties. You may need to take out a specialist listed buildings policy. If you struggle to find a policy, the British Insurance Brokers’ Association may be able to suggest a broker that can help.

There are many factors that affect how much you’ll pay for home insurance, including where you live, the value of your property and any previous claims. Your credit score is unlikely to be one of the main factors affecting your premium – or your ability to get a quote in the first place – but insurers may take it into account. It’s more likely to have an impact if you want to pay in monthly instalments rather than a single annual payment, and if you’re taking out a home insurance policy on a property for the first time rather than renewing.

Choosing the right option

There are calculators that let you accurately estimate the rebuild value of your property and the total value of your contents. The Association of British Insurers has commissioned a rebuild value calculator and many insurers have their own contents value calculators.

Make sure you check the maximum limit to which an insurer is willing to cover any single item, too. For example, while your engagement ring may be worth £15,000, your insurer may only provide up to £3,000 cover for jewellery as standard. If this is the case, you should be able to increase cover for this item. It’ll cost a bit extra, but it’ll be worth it if criminals target your home and steal your jewellery.

If you’re letting out a property you own, it’s your responsibility (not the renter’s) to pay for buildings insurance. You should check that any buildings insurance policy covers you for renting out your property. Even if it does, you may wish to take out dedicated landlord insurance instead. As well as damage to the structure of the building, landlord insurance policies typically also include cover for loss of rental income, personal injury cover if someone is hurt on your property, and cover for your belongings – for example, if you are letting a furnished property.

Not necessarily, although standard buildings insurance will not cover you in the event of someone sustaining an injury on your property, or if you experience a loss of rental income due to damage to the property. If you want to cover these things, you will also need to take out landlord insurance.

If you’re renting the property you live in, your landlord is responsible for insuring the building. They may also have contents insurance for their belongings (such as furniture in a furnished property). You may wish to take out contents insurance to cover your own belongings in a rental property, particularly if you’re providing your own furniture. Some insurers offer dedicated tenants insurance policies, which may also cover common issues that could cause you to lose your rental deposit.

It depends on your specific requirements. Setting a higher voluntary excess will make your home insurance more affordable in the first place, but don’t set it so high that you can’t afford to pay it in the event of a claim. Most people won’t need to claim on their home insurance in any given year. But, if you do, you may regret a too-high excess that eats into your payout. In April to June 2023, home insurers paid out £8.6 million per day to repair homes and replace contents. Find out more about home insurance statistics in our dedicated guide.

As standard, most contents insurance policies only cover items when they’re inside your home. If you want to protect valuables that you carry outside of the home, consider a personal possessions add-on. Some more comprehensive (and usually more expensive) policies may include a level of personal possessions cover as standard.

Under buildings insurance, your policy will typically cover you for the full cost of rebuilding your property if it’s damaged or destroyed (minus any policy excess). With contents insurance, it depends on the terms of your policy. In some cases your contents insurance may make a deduction from the full value of certain items, such as clothes or furniture, to account for “wear and tear”. Check your contents insurance wording carefully. If it offers “new for old” cover for items, you’ll receive the full replacement value.

Not necessarily. If you’re an owner-occupier then it’s probably worth getting cover for both your house and possessions. If you’re renting, you may only want contents insurance to protect your belongings. If you’re a landlord, you can get specialised insurance that covers both the building and any contents in the property that you own. Landlord insurance also protects you from loss of rental income.

As the name suggests, the rebuild cost of your home is how much you’d need to pay to rebuild your property from the ground up if, for example, it was destroyed by a fire. It’s not the same as the sale value of your home, which is usually higher (as this takes into account the value of the land it’s built on). The Association of British Insurers has worked with the Building Cost Information Service (BCIS) of the Royal Institution of Chartered Surveyors (RICS) to create a rebuild cost calculator. You can also hire a professional chartered surveyor to carry out a valuation.

Adjusting your policy

Yes, you should be able to adjust or change your policy. This could be simply because you want a different level of cover. You should also let your insurer know if your circumstances change. For example, if you get a pet, or if you have renovations done that affect the size or structure of your home. Your premium may increase (or, in some cases, decrease), and you may incur an administration fee. The latter depends on your provider.

Yes, but be aware that you will no longer be covered once you cancel your policy. If you have already paid your yearly premium, you will be refunded for the period you didn’t use, minus admin fees.

Some insurers will let you transfer your existing insurance when you move, but they will also likely adjust your premiums based on your new location and the type of house you move to. If this isn’t possible, you may need to cancel your existing policy and take out another one to cover your new residence.

Yes, but you will need to let your home insurer know about any major building work (for example, anything that requires scaffolding). If you don’t, it could invalidate your policy if you need to claim. Make sure you let your insurer know when the building work finishes, too.

Making a claim

Most providers will let you lodge a claim online or via phone. You will generally need to provide your policy number and details of the claim. It’s also a good idea to keep a record of the damage caused, as well as any receipts or invoices for things that are damaged.

Many insurance claims can be settled within a couple of days, at which time you should receive your insurance payout. More complex claims may require that someone from the insurance company inspect your house before approving your claim. They may also need to call in a specialist to check the extent of the damage, which can delay the approval process.

Many home insurance policies offer alternative accommodation cover, which means they will pay for you to find somewhere to stay while your house is being rebuilt or repaired.

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Danny was a publisher at Finder specialising in insurance and investing. He previously worked at the global insurer Aon and has appeared in national media giving advice on insurance. Danny holds a BA in International Business from the University of Plymouth and has undying loyalty to his average-poor football team, Portsmouth FC.

See full bio

Danny's expertise

Danny

has written

292

Finder guides across topics including:

Ceri Stanaway is a researcher, writer and editor with more than 15 years’ experience, including a long stint at independent publisher Which?. She’s helped people find the best products and services, and avoid the pitfalls, across topics ranging from broadband to insurance. Outside of work, you can often find her sampling the fares in local cafes.

See full bio

Urban Jungle offers three kinds of policy: contents insurance, contents and buildings insurance and tenants’ liability, all created with renters in mind.

Looking for home insurance? Use our comprehensive guide to find out if Nationwide offers the right policy for you and start protecting your home and contents by buying online today.

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.