Lenders will look at your credit history if you’re looking to get a credit card or take out a personal loan. Your credit score is a number that represents how creditworthy you are, but what is the average credit score?

Credit score statistics: Highlights

The average credit score in the UK is 644 on the Equifax scale.

More than 1 in 4 Brits (27.2%) fall into the excellent credit score band.

1 in 5 people in the UK (19.8%) have a poor credit score.

An estimated 1 in 10 Brits are credit invisible, meaning they have no credit history – around 5.6 million people.

5% of Brits have admitted to hiding credit score problems from their partner.

What is the average credit score in the UK?

The average credit score in the UK is 644 according to Equifax. The average credit score varies depending on age group and location within the UK. It is also important to note that scores will be different depending on the credit reference agency used.

The averages and figures used in this article are based on Equifax data.

Share your opinions to win prizes or earn cash!

Share your opinions to win!

Sign up to receive deals and tips, plus opportunities to win prizes for your opinions and experiences! (T&Cs)

Credit scores are divided into different bands to help people in the UK better understand their position and rating when it comes to their credit history and how likely they are to be accepted by a lender. There is no such thing as a universal credit score in the UK as there are different credit scoring agencies.

Equifax

Equifax uses a 5-band system ranging from poor to excellent, with a highest possible score of 1000. A good credit score needs to be at least 531.

Poor: 0-438

Fair: 439-530

Good: 531-670

Very good: 671-810

Excellent: 811-1000

Experian

Experian uses a 5-band system ranging from very poor to excellent, with a highest possible score of 999. A good credit score needs to be at least 881.

Very poor: 0-560

Poor: 561-720

Fair: 721-880

Good: 881-960

Excellent: 961-999

Transunion

TransUnion uses a 5-band system ranging from very poor to excellent, with a highest possible score of 710. A good credit score needs to be at least 604.

Very poor: 0-550

Poor: 551-565

Fair: 566-603

Good: 604-627

Excellent: 628-710

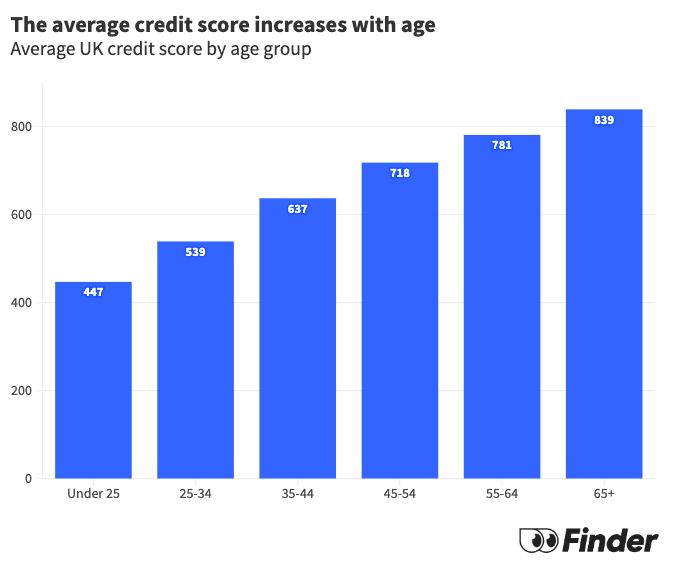

What is the average credit score by age?

18-25 year olds have an average credit score of 447.

25-34 year olds have an average credit score of 539.

35-44 year olds have an average credit score of 637.

45-54 year olds have an average credit score of 718.

55-64 year olds have an average credit score of 781.

65+ year olds have an average credit score of 839.

The average credit score increases with age, according to 2023 data from Equifax. People under the age of 25 tend to have a poor credit rating, while those between the ages of 25 and 44 have a good credit score on average.

Those aged between 45 and 64 have a very good credit rating. Those aged 65 and over are the only people that have an excellent credit score on average.

1 in 5 people in the UK (19.8%) have a poor credit score. 1 in 20 Brits (5%) have also admitted hiding credit score problems from their partner in a current or past relationship.

How many Brits are credit invisible?

Our research in 2023 found that 1 in 10 Brits (10%) would be classed as credit invisible, meaning they have no credit history on record. This equates to around 5.6 million UK adults.

According to Emily Herring, credit and loans expert at finder.com, being classed as “credit invisible” has several downsides: “Credit applications may take longer because lenders will have to complete a manual and detailed risk assessment. The rates you’re offered may also be higher since lenders have no evidence that you’ve been able to manage credit well in the past.”

If you are a young person or you have a limited credit history, you can establish a good credit report by using a credit card.

What is the average credit score in your area?

The average credit score is lowest in Northern Ireland and highest in the South East, with scores of 603 and 680 respectively. There is a significant difference between the regions:

People in Northern Ireland have an average credit score of 603.

People in London have an average credit score of 607.

People in the North East have an average credit score of 613.

People in the North West have an average credit score of 617.

People in the West Midlands have an average credit score of 627.

People in Yorkshire and The Humber have an average credit score of 629.

People in Wales have an average credit score of 640.

People in the East Midlands have an average credit score of 644.

People in Scotland have an average credit score of 649.

People in the East of England have an average credit score of 668.

People in the South West have an average credit score of 671.

People in the South East have an average credit score of 680.

Region

% Split

Average score

East Midlands

8.00%

644

East of England

12.40%

668

London

11.10%

607

Northern Ireland

2.00%

603

North East

3.60%

613

North West

10.50%

617

Scotland

6.70%

649

South East

18.40%

680

South West

6.60%

671

West Midlands

8.30%

627

Wales

4.80%

640

Yorkshire and The Humber

7.40%

629

How many people have an excellent credit score?

This is the breakdown of credit score bands according to data from Equifax:

More than 1 in 4 (27.2%) fall into the excellent credit score band.

Around 1 in 5 people (21.5%) fall into the very good band.

Around 1 in 5 people (20.5%) have a good credit rating.

Around 1 in 10 (11%) have a fair credit rating.

Just under 1 in 5 people (19.8%) have a poor credit score.

To find out how many Brits are credit invisible, Finder commissioned Censuswide on 27/11/2023 to carry out a nationally representative survey of adults aged 18+. A total of 2,000 people were questioned throughout Great Britain, with representative quotas for gender, age and region.

Click here for more research. For all media enquiries, please contact –

Matt Mckenna

UK Head of Communications T: +44 20 8191 8806

Hide

Share your opinions to win prizes or earn cash!

Share your opinions to win!

Sign up to receive deals and tips, plus opportunities to win prizes for your opinions and experiences! (T&Cs)

Sophie Barber is a senior content marketing manager for Finder in the UK. She has over 5 years experience in writing and publishing clear, concise and informative articles that help consumers make informed decisions.

See full bio

Sophie's expertise

Sophie

has written

97

Finder guides across topics including:

Kate Steere is an editor and money expert at Finder, specialising in banking, savings and fintech. She has previously written for The Motley Fool UK and Fitch Solutions, where she covered a wide range of personal finance topics and kept a close eye on market trends. Kate has a Bachelor of Arts in Modern History from the University of East Anglia. When not working, she can usually be found curled up with a good book or heading out for a run.

See full bio

Kate's expertise

Kate

has written

160

Finder guides across topics including:

Discover how to supercharge your points through everyday spending – plus a few ways to redeem them with the American Express® Preferred Rewards Gold Credit Card. (Paid content)

Get all the details on how we rate the credit cards we review. We look at costs, fees, features and how well a card performs compared to the rest of the market.

Buy now and pay interest later with a 0% purchase credit card. Compare current offers with 0% p.a. on purchases.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.