App-based Countingup is a business current account with built-in accounting software. It’s designed to let small business customers pay their bills, issue invoices and do their accounting all from the same app.

What is Countingup?

Having launched in January 2018 for freelancers and sole traders, the business e-money account is now also available for limited companies. Countingup says it reached 8,000 customers during its first year, and that it’s now used by over 50,000 businesses.

Countingup isn’t a bank, but the account is provided through an e-money institution that’s authorised by the Financial Conduct Authority (FCA).

How does Countingup work and what are its features?

Signing up to Countingup takes a matter of minutes. If you are 18 or over, have a business registered in the UK and are a UK resident, these are the features Countingup offers you:

Business current account. You can send and receive money transfers, make payments and set up direct debits.

Prepaid card. It’s a contactless Mastercard, so you’ll be able to pay pretty much everywhere.

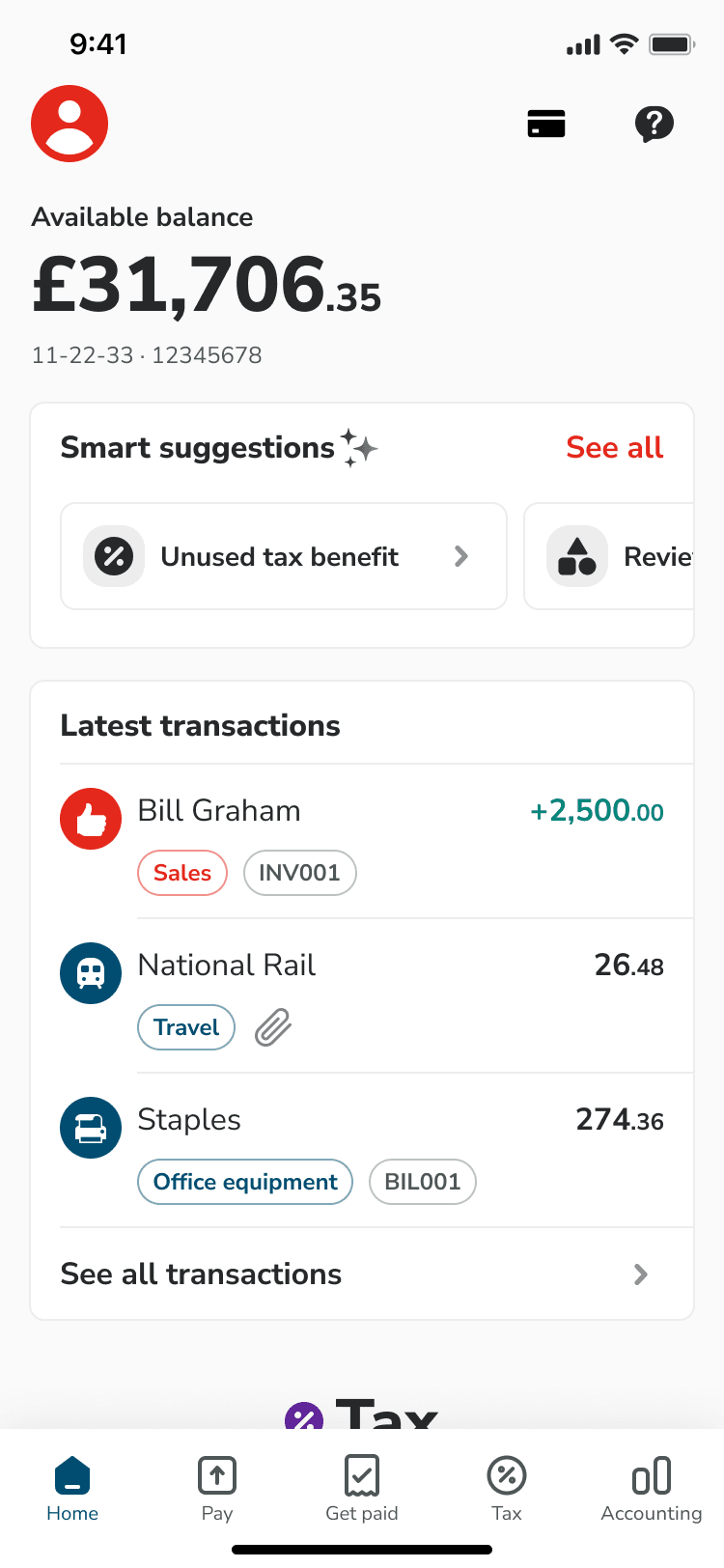

App. That’s where you manage your account and where you’ll find all the accounting features, including automated bookkeeping and invoicing. For now, you can’t do it from a desktop.

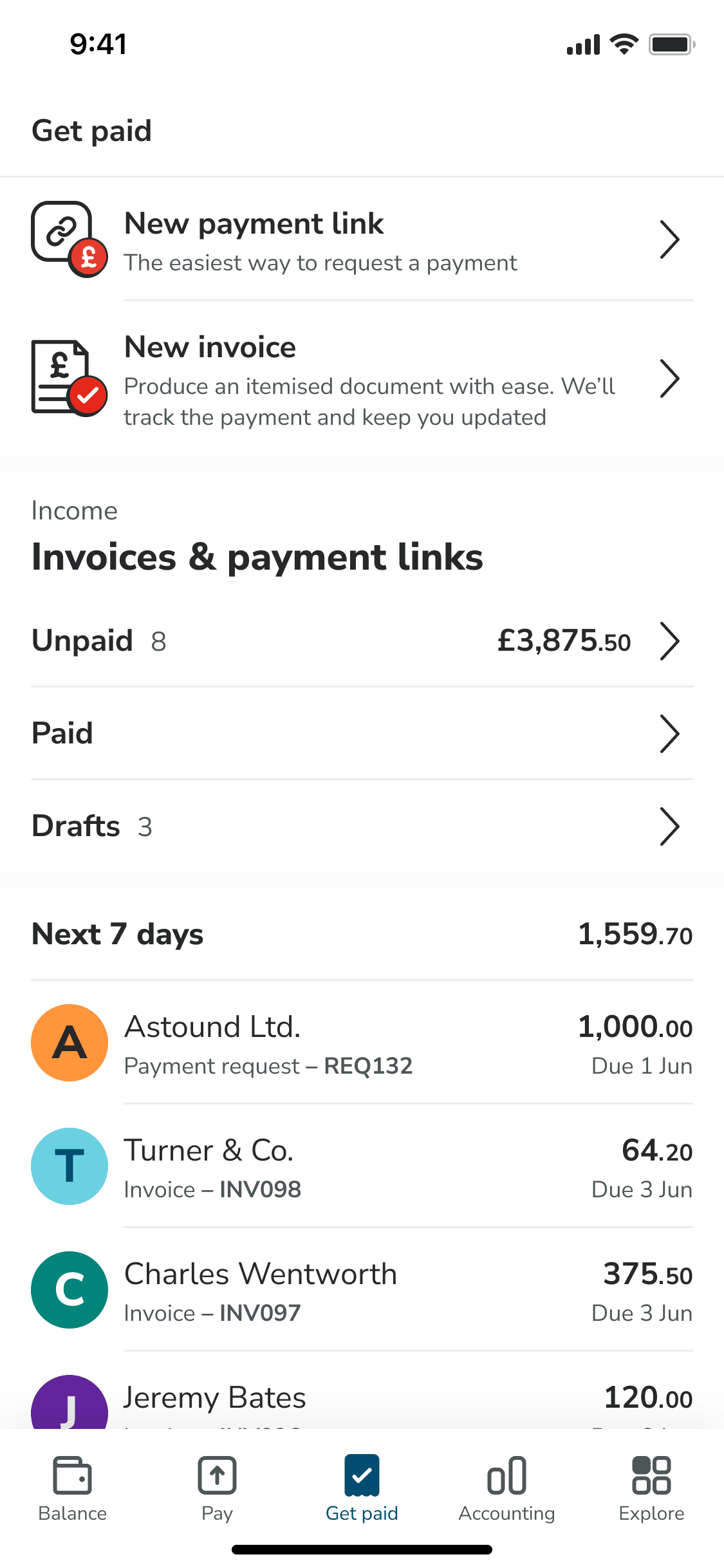

Invoicing. You can create invoices and, once paid, Countingup will automatically match them to the corresponding transaction (provided that the invoice number is referenced and the amount is the same).

Expense capture. You can add a picture to each of your payments in the app, with the idea of attaching photos of your receipts for future reference.

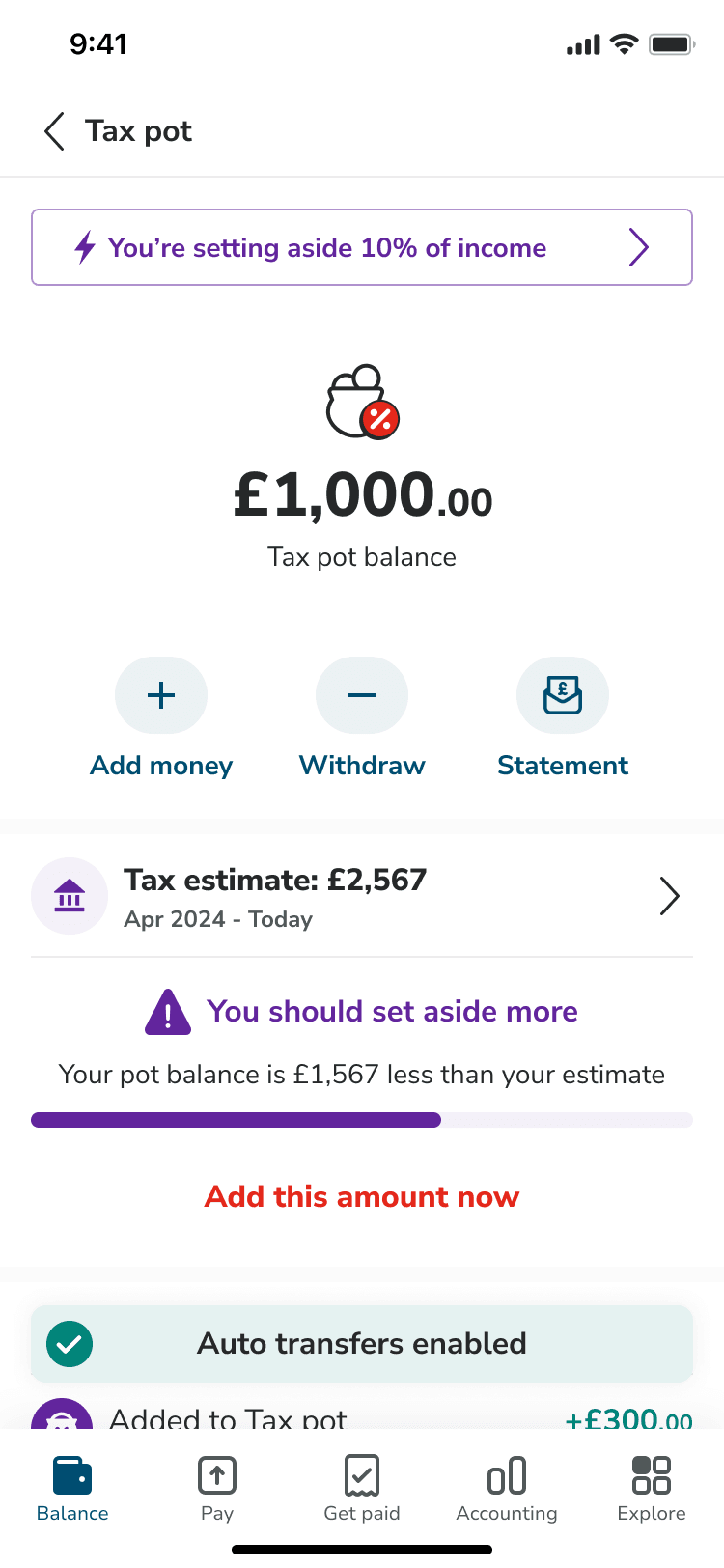

Tax calculations. Work out your tax bill and how much you should set aside to pay it.

Profit and loss. Instantly see how your business is performing, based on income and outgoings from the account.

Share with your accountant. Invite your own accountant to digitally view receipts and statements.

Countingup fees

There are three tiers of monthly membership for a Countingup account:

£3 a month. Tier one for people who pay in under £750 a month.

£9 a month. Tier two is for businesses with deposits of between £750 and £7,500 a month.

£18 a month. Tier three is for accounts with incoming funds of more than £7,500 a month.

Those prices are not all-inclusive. All tiers are also charged the same fees for most account services including:

Bank transfers. 30p each, both to make and to receive them.

ATM withdrawals. £1 each.

Cash deposits. 0.5% of the transaction value at the Post Office (min. £2), 3% of the transaction value at PayPoints.

Currency exchange. The foreign currency transaction fee is 3%.

When signing up to Countingup, you get the first three months for free. That means no monthly subscription fees or bank transfer charges, but all the other transaction fees still apply.

Is Countingup suitable for my business?

Countingup has been created with small and one-person businesses in mind. Its features aren’t tailored for big and complex businesses that employ many people and will be regularly banking tens of thousands of pounds.

Countingup’s main attraction is that it combines accounting with a current account, so you’ll get the most out of the app if you’re planning to use it for both of these things. To enjoy Countingup to its fullest you might be a freelancer or a startup, or a small business that has not established your banking and accounting systems anywhere else yet. Otherwise, you’ll have to be ready for quite a big change in the way you do things, and be prepared to switch over from both your existing business current account and accounting software package.

However, Countingup’s account is an e-money account provided through a company called Prepay Technologies, which is authorised and regulated by the FCA. As an e-money institution, the company must keep your money in a segregated “safeguarding” account – it’s at Barclays, in this case. This means that if the company were to go bankrupt, your deposits couldn’t be used to repay its creditors. However, while there’s no cap on the amount safeguarded this way, you might not get all your money back as administrators are allowed to deduct costs in the event of bankruptcy.

Because Countingup isn’t a bank, your money won’t be protected by the Financial Services Compensation Scheme (FSCS). This means if Countingup went bust you could lose your deposit.”

Customer reviews

Countingup has an average rating of 4.7 out of 5 from around 3,200 reviews on the App Store, while over on Google Play it has an average score of 4.3 out of 5 from more than 1,400 Android app users (updated March 2025).

On Trustpilot, Countingup received a score of 4 out of 5, and a rating of “Great”, from around 2,800 feedback posts. Overall, reviewers on this platform praised the smooth account opening process and account features, although some customers said they would like the option of having more than one bank card with their account (updated March 2025).

Countingup rates and fees

What does the Countingup app look like?

Pros and cons of Countingup

Pros

Quick and easy online set-up.

Combines a current account with accounting.

Free trial available.

You can deposit cash into the account at Post Offices and PayPoints.

Cons

Monthly fees and transaction fees.

Your money isn’t protected by the Financial Services Compensation Scheme.

No overdraft options.

Can’t pay in cheques.

Customer service information for Countingup

Email support

Telephone support

In-app or live chat

Contact form

Branch support

Our verdict: Is Countingup any good?

Integrated accounting in a business account is obviously a great idea, and one that can save small businesses much time and potentially also quite a lot of money, as they don’t have to pay for separate accounting software. However, if you are a freelancer or run a very small business you may not need the accounting facilities Countingup offers.

Countingup’s features are smart and handy, covering off the basics of what you would expect from both a business current account and accounting software. It’s a slick app but it is not a bank and as such isn’t covered by the Financial Services Compensation Scheme. This is a cause for concern as it means if Countingup went bust you might not get all your money back.

When it comes to pricing, there are both monthly account fees and banking transaction fees involved. Some of Countingup’s digital banking competitors do have cheaper prices for these aspects of a business account.

However, let’s not forget that there aren’t many accounting and banking app combos around yet, so this is a relatively unique service at the moment.

Get started by visiting Countingup’s website and sign up for an account. If you have read this review and decided that Countingup’s account is not for you, you can also compare other business bank accounts.

“There are a lot more banking providers offering digital-only business accounts these days,” says Matthew Boyle, Finder’s banking publisher. “If you want to find out more about the business accounts on offer from both the digital challengers and the high street banks, then head over to our business banking section.”

Frequently asked questions

Limited businesses have a £400,000 balance limit, while for those who are self-employed the balance limit is £60,000. All account holders can withdraw a maximum of £500 a day from ATMs.

No, it doesn’t. Countingup is a type of prepaid account, so it doesn’t earn any interest nor can you go overdrawn.

You can do it via bank transfer or by depositing cash into it. You will pay fees in both cases, but bank transfers are way cheaper and more practical.

Countingup was founded by current CEO Tim Fouracre after he stepped down as CEO of Clear Books plc, which was another accounting solution business he founded in 2008.

We show offers we can track - that's not every product on the market...yet. Unless we've said otherwise, products are in no particular order. The terms "best", "top", "cheap" (and variations of these) aren't ratings, though we always explain what's great about a product when we highlight it. This is subject to our terms of use. When you make major financial decisions, consider getting independent financial advice. Always consider your own circumstances when you compare products so you get what's right for you. Most of the data in Finder's comparison tables is provided by Defaqto. In other cases, Finder has sourced data directly from providers.

Michelle Stevens is a deputy editor at Finder, specialising in banking, credit, loans and mortgages. She has a journalism degree from the University of Sheffield and has been a journalist for 15 years, writing on topics including fintech, payment systems and retail. In her spare time, Michelle likes to travel, explore new foodie experiences and attempt to improve her own culinary skills.

See full bio

Michelle's expertise

Michelle

has written

81

Finder guides across topics including:

By switching your business bank account, you may be able to reduce your monthly fees or take advantage of different features like smart bookkeeping tools.

Learn more about the key differences between the Tide and Revolut business bank accounts and which is likely to suit you better.

Advertiser disclosure

Finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which Finder receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. Finder compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.