- Required time in business: 6+ months

- Required annual revenue: $60k+

- Min credit score: 600+

Fundera business loans

Get connected with short-term funding, SBA loans, lines of credit and more.

| Features |

|

|---|

Your options for borrowing money for your business go beyond a traditional term loan to include lines of credit, merchant cash advances and other types of business loans. The business financing you choose should depend on your business and why you need the money.

All responses are collected anonymously and used for internal data purposes only.

What is your primary need for a business loan?

A business loan is any type of financing that’s used to fund business expenses — from paying staff wages and purchasing inventory to expanding your business or improving cash flow to investing in marketing or covering unexpected emergencies.

Startups and entrepreneurs can look to traditional lenders like banks and credit unions as well as online lenders, crowdfunding sites and the Small Business Administration for business funding. Requirements, rates and terms depend on the lender and your business.

Your business typically needs to be at least six months old and bring in over $50,000 a year in revenue to qualify. Other factors like your personal credit score and relationship with the lender also play a role.

Depending on the type of financing, you can find unsecured options that don’t require collateral or secured loans backed by your business assets or the item you’re purchasing. Interest rates can be fixed or variable, with repayment terms lasting anywhere from six months to 25 years.

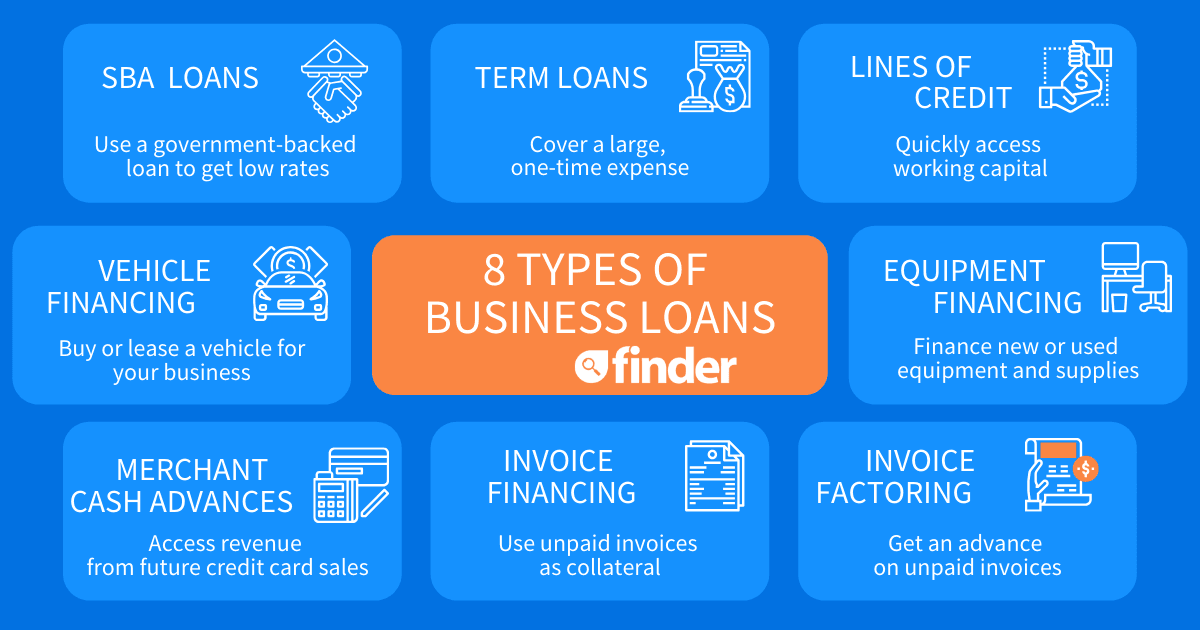

There are several types of financing that you can use to start a business, pay for vehicles or equipment, access working capital and more. Each comes with varying interest rates and loan repayment terms.

Business term loans offer a lump sum you repay in installments plus interest and fees. Term loans come in short-term and long-term loan options. They’re best for funding a one-time expense, like buying a piece of equipment or purchasing a new business.

Term loans can either be secured with collateral or unsecured. But even unsecured business loans typically require a personal guarantee from the business owner.

A business loan marketplace like Lendio allows you to compare term loan offers from multiple lenders.

A business line of credit gives your business cash access as needed to cover working capital expenses. It’s a good option if you have a seasonal business, regularly need funds to purchase inventory or want to have funds available for unexpected expenses. Like a term loan, a business line of credit can require collateral or be unsecured.

Most business lines are revolving credit, meaning that the credit limit replenishes as you pay it off. Typically, each withdrawal turns into a short-term loan, though some lenders might only require minimum monthly payments on your balance. A marketplace like Lendio offers lines of credit from different lenders.

The Small Business Administration (SBA)’s government-backed business loan programs are designed to help small businesses access funding. SBA loans offer low rates and high loan amounts to businesses that are too small or too new to qualify for your typical bank loan. These are usually secured with collateral.

Several different SBA loan programs cover almost every type of expense, from working capital to buying commercial real estate. SmartBiz, our best choice for SBA loans can help you find the right loan for you by simplifying the application process

Whether you need to finance a vehicle or the equipment necessary to run your business, you may be able to finance these expenses 100%, depending on your business credit score and monthly revenue.

This type of financing typically offers fixed-rate installment loans that use the purchased vehicles or equipment as collateral. But, depending on the kind of business you run, a vehicle or equipment lease may work better for you.

National Funding, a lender that specializes in this kind of loan, is our pick for best equipment financing lender.

Companies with large amounts of credit card sales may consider merchant cash advances for their business financing. These advances offer quick access to revenue from sales and then require a fixed-charge repayment based on a percentage of your sales. Merchant cash advances can be set up as daily or weekly financing.

If your business cannot qualify for other types of business financing, merchant cash advances can provide a temporary cashflow solution. Importantly, you can get your funding quickly, but it can be one of the more expensive business financing options out there.

Consider a company like Fora Financial, which offers cash advances from $5,000 up to $750,000 if you’ve been in business for at least a year.

There are many differences between business loans and investors. But first, let’s define an investor. An investor is a person or organization who provides funding for your business in exchange for a share of the company, with hopes that they’ll get a return on their money.

Typically, you’ll have several types of investors to choose from. No matter which you choose, you’re indefinitely giving up a slice of your company’s value — called equity — in exchange for funding.

Invoice financing and factoring offer an advance on unpaid customer invoices. Invoice financing is generally available for invoice volumes under $20,000, though invoice factoring can run from around $20,000 to $10 million. Instead of interest, you pay a monthly or weekly fee based on the time it takes for customers to fill their invoices. These fees can be high compared to the interest you might pay on your typical business term loan or line of credit.

Invoice financing allows you to maintain control of your unpaid invoices and offers up to 100% of the invoice value upfront. Invoice factoring involves selling unpaid invoices to a company. The factoring company usually offers 85% to 95% upfront and the rest, minus a fee, after your customers fill their invoices.

Our choice for the best invoice financing and factoring lender is FundThrough, which offers up to 100% of your accounts receivables.

The debt service coverage ratio — more commonly called the DSCR — is an industry measure of the cash income a business has left over at month’s end that can be used to service its debt. It includes principal, interest and lease payments.

The DSCR is a main benchmark used to determine your ability to repay a loan. When you apply for a loan at a bank or credit union, the lender uses your DSCR to decide whether your business can manage its repayments. If your business isn’t generating the income it needs to pay its operating costs and make repayments, then a lender will likely pass on your application.

Calculate your DSCR by dividing your annual business operating income by your total annual debt service level — the amount of principal and interest you must repay in a given year. The total annual debt service level will include your current debt and the loan you’re applying for.

A lender may use a different figure when assessing your operating income. Some use the earnings metric called EBITDA — or earnings before interest, taxes, depreciation and amortization — while others add net operating income to depreciation and any other noncash charges.

As a result, the DSCR figure won’t be the same across lenders, which can make a direct comparison among them difficult. Some also express the DSCR as a percentage rather than as a ratio.

A closer look:

The type of loan you get and the lender you work with are the biggest factors that determine how much you can borrow with a business loan. And you might find easier approval with a business loan backed by a form of collateral — be it a car, a tractor or your business’s future sales. A secured loan is less risky for the lender, who can sell your collateral to soften the financial hit if your business defaults.

In a sole proprietor, a single person owns and runs an unincorporated business. While a sole proprietor can have employees, they are the only ones paying income tax on profits earned.

Because sole proprietors have little separation between business and personal finances, banks and other financial institutions often view them as risky investments. If a sole proprietor loses out on an important contract, gets sick or cannot continue their business for any reason, the lender has wasted money on a loan that will likely go unpaid.

This risk makes it difficult for sole proprietors to secure a business loan, but it’s not impossible. With the right documentation and a good business plan in place, there are lenders willing to offer loans to sole proprietors.

| Loan types | Typical amounts | How it works | Pros and cons |

|---|---|---|---|

| SBA loan | $5,000–$5 million | An SBA loan is backed by the government. Although these loans are harder to qualify for, they’re designed for small businesses with just a few employees and target borrowers who’ve had trouble getting a traditional loan elsewhere. |

|

| Personal loan | $2,000–$100,000 | A personal loan can be used for business expenses. The borrowing amounts are typically lower, and it’s harder to deduct the cost on your taxes. |

|

| Invoice financing | 80% of the invoice amount | Invoice financing gives you an advance on your unpaid invoices. Costs are typically a percentage of the invoiced amount, and you’re expected to pay the advance back quickly after your invoice is due. |

|

| Line of credit | $5,000–$1 million | A line of credit allows you to draw from your credit limit whenever you need, and you only pay interest on the money you borrow. |

|

| Term loan | $2,000–$5 million | A term loan allows you to borrow a single lump sum and pay it back over time. |

|

Consider this scenario: Sarah is a self-employed landscaper who designs boutique gardens for wealthy homeowners and small businesses across Seattle. She employs a part-time assistant and hires landscapers on a project-by-project basis.

Recently, a large hotel chain contracted her to design and build a courtyard garden for a new property. While promising, this is a much bigger job than her usual projects, and she realizes she needs at least $60,000 to hire more laborers and rent equipment.

Sarah’s choice: A term loan

With a good idea of her costs and safety knowing her client is large and stable, Sarah opts for a term loan from a bank. Because her business has been in operation for years, she’s able to get a fixed repayment plan with a low interest rate of 9.25%.

Veterans may get specialized loan programs designed to support and empower military veterans in their entrepreneurial endeavors. Some business loans for veterans may come with favorable terms and conditions, such as lower interest rates, flexible repayment options, and reduced or waived fees.

You may also be able to take advantage of small business grants and veteran entrepreneurship programs through the SBA — or get a line of credit, equipment loan or accounts receivable loan from a bank or online lender.

Even if you’ve been in business for years, have excellent credit and are turning a profit, your business still might struggle to qualify for a loan if it’s part of a high-risk industry.

Lenders generally consider industries high risk if they are more likely to fail. For example, industries like alcohol and gambling might be considered high risk because they’re subject to regulations that frequently change. However, other industries like restaurant and retail might be seen as risky because revenue isn’t always guaranteed.

Examples of high-risk industries include:

If you own a high-risk industry and can’t get approval from traditional lenders, you can find other types of financing, though they tend to be expensive.

If you’re looking to expand your business through advertising, you can use a business loan to fund a marketing campaign in some cases. It helps to nail down your marketing strategy before you apply for financing.

Here are some common ways marketing loans can be used.

It may seem like every online lender offers the same thing, but that doesn’t make it true. Like any loan option, compare the features of the loan and the rules set by the lender to get the best online business loan that offers the most for your money. The brands listed below have some features in common, giving you a solid way to kick off the comparison process.

A no-credit-check business loan is a type of business financing where the lender doesn’t consider your credit score during the application process. It’s typically short-term financing and can cost more than other options.

Often, no-credit-check business loans don’t work like a typical unsecured term loan. Most require some kind of collateral or a personal guarantee. Others might consider different risk factors, like your clients’ credit scores.

It’s possible but not likely. Most startup-friendly loans tend to rely on the business owner’s credit to make up for the fact that your business doesn’t have a long record of revenue.

Unless you have enough money in a retirement plan to fund a new business with a ROBS, you might have difficulty finding a legitimate lender willing to forego a credit check completely. Here’s how startup funding works by credit score:

It depends on what you need to finance. Business loans are designed to cover a large one-time expense and you’ll have low-interest business loan options to choose from depending on youor credit, while credit cards are designed to cover smaller expenses that are hard to predict over a long period.

It also depends on your cash flow. If you have the cash flow to pay off your credit card balance each month, you won’t have to pay any interest.

Some credit cards come with a 0% APR promotional period, which can last as long as 12 months. If you pay off the balance before the period is up, you won’t have to pay interest.

| Compare business credit card if you … | Compare loans if you … |

|---|---|

|

|

Most small businesses can get a business loan by determining how much funding the business needs and comparing lenders. Qualifications generally include:

If you don’t meet qualifications, you may be able to find financing from an SBA loan provider or an alternative lender if bank loans aren’t an option. Alternative lenders include microlenders, online business loan providers and factoring companies. They might not offer competitive rates compared to a bank, but they can help your business get to a place where it’s eligible for a bank loan. You may even be able to find some loan options without having any money or revenue yet.

The turnaround time for a business loan largely depends on the lender you work with and the type of financing you’re interested in. It can take a bank or credit union one to two weeks to process a business loan application and disburse your funds.

Alternatively, online lenders may be able to offer you an instant approval decision and fund your loan within a few business days, while others may be able to offer loans with same-day funding. And with SBA loans, the entire process can take several months.

Before you start comparing lenders, calculate how much you need to borrow, assess the state of your business’s finances, check your personal credit report and choose the type of financing you need.

Once you have a better idea of what you need, look for lenders offering the loan amount and type of financing you need — with basic requirements that your business meets.

Then, compare the rates, fees, terms and turnaround time for each product. You might want to weigh other factors that are important to you, like no paperwork requirements or lower rates for repeat borrowers. If you’re applying online, you may also want to consider the steps lenders take to protect applicants’ information.

Using a lending marketplace like businessloans.com or Lendio may also offer a way for you to quickly compare multiple loan offers from top lenders with just one form.

Not ready to take out a business loan just yet? Consider one of these alternatives:

Crowdfunding is a way to raise a one-time sum that doesn’t need to be repaid. There are several types of crowdfunding, though seed funding — or rewards-based crowdfunding — and equity crowdfunding are common options. Both typically take around a month to raise the funds you need and are great for exciting projects.

With rewards-based crowdfunding, your business sets up an online campaign to raise money from fans, family and friends and offers prizes in return for donations. With equity crowdfunding, your company raises money from investors in exchange for a share of ownership in your business.

Crowdfunding is ideal for businesses that have an exciting or profitable project on the horizon. But there are some situations where you may want to think twice.

Peer-to-peer (P2P) lenders fall somewhere between a type of business loan provider and a crowdfunding platform. These lenders work like a crowdfunding platform to connect you with investors who want to profit from your business’s interest payments.

But the actual process of applying, getting approved and repaying your loan works more like a business loan. You rarely need to submit a pitch deck or marketing video. And your credit score, time in business and revenue usually matter.

And peer-to-peer business loans typically aren’t as fast as loans from direct online lenders, however, since you often have to wait for investors to fund your loan. With LendingClub, one of the top P2P lenders in the country, the whole process can take several days from the time you’re approved.

Explore the top business loan guides to help you along your business journey. From information on the best business loans on the market or your best startup loan options, to business loans that require little to no paperwork and more.

Best financing options for trucking companies to cover licensing, new trucks, insurance, vehicle maintenance and more.

Think you need a cosigner for your business loan? Learn when they help — and when they don’t.

Get connected with short-term funding, SBA loans, lines of credit and more.

Business loans that don’t require a personal guarantee, including options for comparing multiple lenders and specific loan types.

Compare $50,000 no-doc business loans for an expedited lending process.

Compare different lenders to secure a $400,000 business loan with favorable terms.

Buy real estate, another business or expand your enterprise.

You’ll have an easier time qualifying if you have strong credit and high revenue.

Find financing to grow your business — or even buy another.

Stay away from big banks for a loan of this size.