Where can I find my current mortgage balance?

Find the exact amount of mortgage balance on your monthly statement or in your online mortgage account. Contact your lender if you have trouble finding it.

Home equity is the difference between your current mortgage — if you have one — and your home’s fair market value. Calculating how much equity you have in your home lets you see how much cash you can potentially borrow with a home equity loan, home equity line of credit (HELOC) or cash-out refinance. This money can be used for any purpose, such as paying for home renovations or to consolidate higher interest debt.

Calculating your home equity is a straightforward matter: Subtract what you owe on all the secured debt against your home from its appraised value.

Secured debt may include:

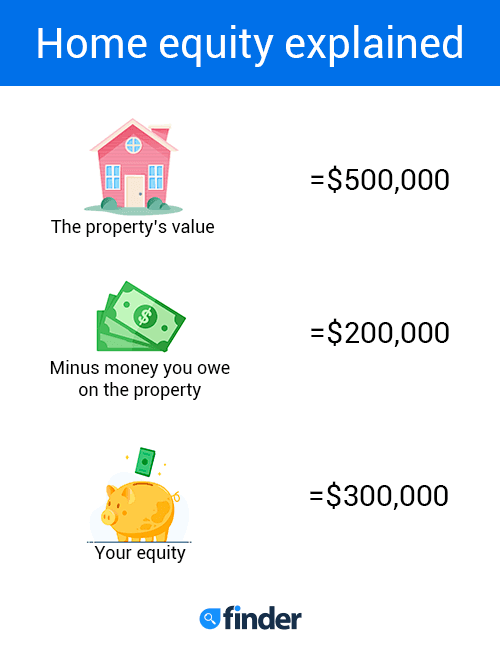

For example, if a recent appraisal shows that your home is worth $500,000 and you owe $200,000 on your current mortgage and you have no other secured debt against your home, your home equity is $300,000.

Find the exact amount of mortgage balance on your monthly statement or in your online mortgage account. Contact your lender if you have trouble finding it.

Even if you have $200,000 worth of equity in your home, you likely won’t be able to borrow the full $200,000. That’s because lenders use something called the loan-to-value (LTV) ratio and combined loan–to-value (CLTV) ratio to determine how much you can borrow.

LTV and CLTV are similar, but the differences are:

Most lenders lend at 80% CLTV when you get a home equity loan or HELOC, but some may go higher — even up to 97% CLTV — depending on your creditworthiness.

Calculate LTV using this formula:

LTV% = (Current loan balance ÷ Home’s appraised value) x 100

Calculate CLTV using this formula:

CLTV% = (Current loan balance + Home equity loan or HELOC ÷ Home’s appraised value) x 100

See our HELOC calculator to quickly calculate how much you might be able to borrow against your home with a home equity loan or HELOC.

Most lenders require that you pay for PMI while your home’s equity is below 20%. However, if the lender cancels your PMI before you get a home equity loan, the servicer can’t require further PMI payments more than 30 days after the termination date.

Theoretically, this means you could get a home equity loan that pushes your equity below 20%, but you don’t need to pay PMI on your primary mortgage once it’s been canceled. Please consult with your lender if you have any questions about PMI requirements.

Your home equity is only one number lenders look at when you want to refinance your mortgage or take out a home equity loan. They also look at your FICO credit score, your debt-to-income ratio (DTI) and your income.

While getting a home equity loan or HELOC is often cheaper than a cash-out refinance mortgage, there are costs to consider. Here are the costs and fees you’re most likely to run into on a home equity loan or HELOC:

Closing costs, origination fees and other expenses — if any — can affect the cost of your loan and reduce the total amount of home equity you have. If you must pay these fees, be sure that the trade-off in the form of lower interest rates or faster loan funding is worth it to you.

Use our tool to get personalized estimated rates from top lenders based on your location and financial details. Select whether you’re looking for a Home Equity Loan, HELOC or Cash-Out Refinance.

If you selected a home equity loan or HELOC, enter your ZIP code, credit score and information about your current home to see your personalized rates.

In the Cash-Out Refinance tab, select Refinance and enter your ZIP code, credit score and other property details to see what you might qualify for.

Here are some strategies to increase the equity in your home:

Now that you know how to calculate your home’s equity and your loan’s LTV, you may be ready to compare home equity loan lenders and HELOCs or learn more about cash-out refinancing to determine which is the right choice for you. If you’re unsure about drawing upon your equity at this point in your mortgage, consult a professional financial advisor.

Together, these 7 HELOC lenders cater to a diverse range of borrowers.

Learn more about the rates, terms and support you can expect from lenders in the US to empower you when shopping for a home equity loan.

Use this calculator to estimate your monthly payment for a home equity loan.

Borrow up to $1 million with PenFed’s sole home equity product.

Access your equity through a partnership that shares in your home’s appreciation — or not — over 10 years.

Learn about how HELOCs work, how it’s paid back, fees, pros and cons, and more.

Our list of this year’s best home equity loan lenders. These lenders cater to particular types of borrowers, from military members to those with fair credit.

This complex strategy may save you money in the long run but it can be risky.

It varies, but be prepared to gather documentation and verify your financial situation.

Use your equity to get a flexible credit line, if you can qualify.